Short Answer

If you retire before Medicare, you need a health insurance bridge.

For many people, the options include:

- A spouse's employer plan

- Retiree health coverage

- COBRA

- Marketplace coverage

- Private coverage outside the Marketplace

- Medicaid, if eligible

HealthCare.gov says that if you retire before age 65 and lose job-based health coverage, you can use the Health Insurance Marketplace to buy a plan. Losing job-based coverage can qualify you for a Special Enrollment Period.

The planning problem is that healthcare costs are not separate from retirement income. IRA withdrawals, 401k withdrawals, Roth conversions, capital gains, and part-time work can all affect income, and income can affect Marketplace savings.

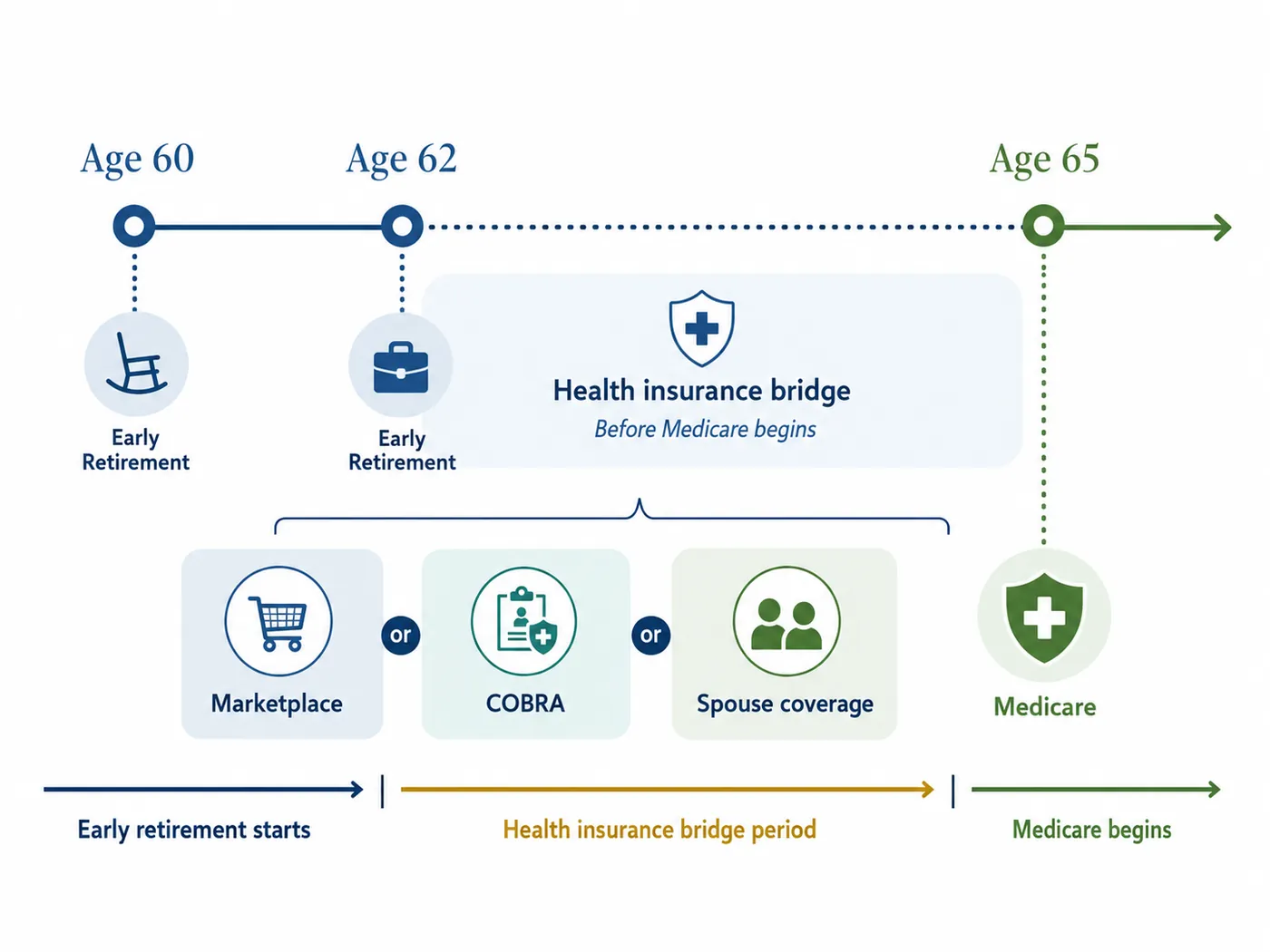

Why The Healthcare Bridge Matters

For many early retirees, healthcare is the question that decides whether retirement is realistic.

A portfolio may look strong before healthcare is included. Then premiums, deductibles, out-of-pocket costs, prescriptions, and income-based subsidy rules change the answer.

The bridge period can be short or long:

- Retire at 64: about one year before Medicare

- Retire at 62: about three years before Medicare

- Retire at 60: about five years before Medicare

- Retire at 55: about ten years before Medicare

The longer the bridge, the more important the healthcare model becomes. If you are weighing an age-62 exit, can I retire at 62 before Medicare? covers the bridge-year decision.

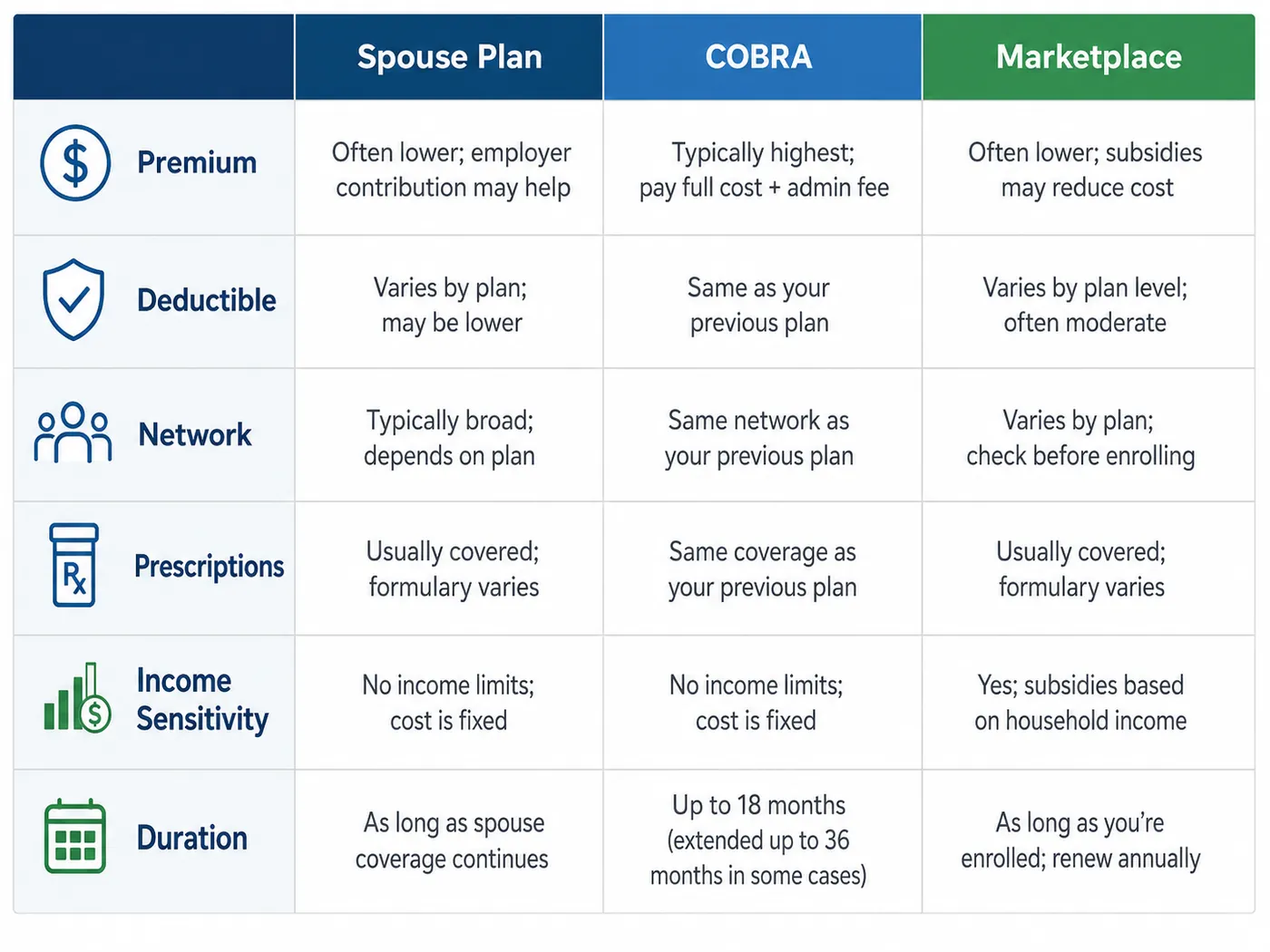

Option 1: A Spouse's Employer Plan

If one spouse keeps working, joining that spouse's employer plan may be the simplest bridge.

Questions to ask:

- Can the retired spouse join the plan?

- What is the employee plus spouse premium?

- Are doctors and prescriptions covered?

- How do deductibles and out-of-pocket limits compare?

- Does the working spouse plan to retire before age 65 too?

This option can reduce uncertainty, but it may depend on one spouse continuing to work longer than planned.

Option 2: Retiree Health Coverage

Some employers offer retiree health benefits. HealthCare.gov says if you have retiree coverage and want to buy a Marketplace plan instead, you can, but premium tax credits and other savings may not be available if you are actually enrolled in retiree coverage.

That makes retiree coverage a comparison problem:

- Monthly premium

- Deductible

- Out-of-pocket limit

- Network

- Prescription coverage

- Eligibility rules

- Whether spouse coverage is included

- Whether dropping coverage affects future options

Do not compare premiums alone. A cheaper premium can still be expensive if the deductible, network, or drug coverage is poor.

Option 3: COBRA

COBRA can let some workers and families continue group health coverage after certain events.

The U.S. Department of Labor says COBRA gives workers and families who lose health benefits the right to choose to continue group health benefits for limited periods under circumstances such as job loss, reduced work hours, transition between jobs, death, divorce, and other life events.

DOL also says qualified individuals may have to pay the entire premium for coverage, up to 102 percent of the cost to the plan.

COBRA can be useful because it may preserve the same plan for a limited period. It can also be expensive.

HealthCare.gov notes that if COBRA runs out outside Open Enrollment, you may qualify for a Special Enrollment Period. But choosing to drop COBRA outside Open Enrollment does not automatically create a Special Enrollment Period to enroll in Marketplace coverage.

Option 4: Marketplace Coverage

Marketplace coverage is often the main option for early retirees without employer or retiree coverage.

HealthCare.gov says when you fill out a Marketplace application, you can find out if you qualify for a private plan with premium tax credits and lower out-of-pocket costs, based on income and household size. You can also find out if you qualify for Medicaid in your state.

That means income planning matters.

HealthCare.gov also says savings are based on your income estimate for the year you want coverage, not last year's income.

For early retirees, income may include:

- IRA withdrawals

- 401k withdrawals

- Roth conversions

- Taxable interest

- Dividends

- Capital gains

- Part-time work

- Pension income

- Social Security, if claimed before Medicare

HealthCare.gov specifically notes that IRA or 401k withdrawals generally count as income.

The Roth Conversion Trap

Roth conversions before RMD age can be useful. They can also raise income during pre-Medicare healthcare years.

That matters because Marketplace savings depend on income and household size.

For example, a retiree might convert $40,000 from a traditional IRA to Roth in a low-wage retirement year. From a tax-bracket view, that may look reasonable. From a healthcare view, it may reduce premium tax credits or cost-sharing reductions.

The answer is not "never convert before Medicare."

The answer is:

Model the conversion and the healthcare cost in the same plan. A retirement calculator with taxes and healthcare is built to do exactly that.

The IRA Withdrawal Problem

If you retire before Social Security and Medicare, you may need portfolio withdrawals to cover your retirement spending.

The source of those withdrawals matters.

A retiree might spend from:

- Cash

- Taxable brokerage

- Traditional IRA

- 401k

- Roth IRA

Some withdrawals may raise income more than others. A traditional IRA withdrawal generally affects taxable income. A qualified Roth withdrawal may not. A taxable account sale may create capital gains.

Because Marketplace savings can depend on estimated household income, withdrawal order can affect healthcare costs.

This is why the healthcare bridge is also a drawdown strategy. See which retirement account should you withdraw from first?

Medicare Starts Later, But The Plan Starts Now

Medicare.gov says most people get Medicare Part A and Part B when first eligible, usually when turning 65. It also says the date Part A and Part B coverage starts depends on when you sign up.

That means early retirees need two plans:

- A bridge plan before Medicare

- A Medicare enrollment plan at 65

HealthCare.gov says you can get a Marketplace plan before Medicare begins and cancel it once Medicare coverage starts.

Do not assume the Marketplace plan automatically solves the Medicare transition. Put the Medicare date into the plan.

A Simple Example

Suppose a couple retires at 62.

They need three years of health insurance before Medicare. They have:

- $900,000 in retirement savings

- Cash savings

- A traditional IRA

- A Roth IRA

- Taxable brokerage

- Social Security planned at 67

- No retiree health coverage

They compare three healthcare paths:

- COBRA for a limited period, then Marketplace coverage

- Marketplace coverage immediately

- One spouse works part-time for employer coverage

Then they compare income strategies:

- Spend cash first

- Use taxable brokerage first

- Take modest IRA withdrawals

- Do Roth conversions before Medicare

The best healthcare path may depend on the income strategy. The best income strategy may depend on the healthcare path.

That is why these choices need to be modeled together.

How To Model Pre-Medicare Healthcare In The Planner

Use this workflow in the AI Retirement Income Planner:

- Enter retirement age and Medicare age.

- Add estimated healthcare costs for the bridge years.

- Enter account balances by type: cash, taxable, tax-deferred, and Roth.

- Add expected Social Security claiming ages.

- Use Tax & ACA to review income-sensitive healthcare effects.

- Set which accounts fund each phase using the per-phase withdrawal fields (that per-phase mix is your withdrawal order).

- Use What-if? to compare Roth conversions or IRA withdrawals.

- Use Scenarios to compare COBRA, Marketplace, spouse coverage, or delayed retirement.

- Run Stress test for high healthcare inflation or market weakness.

- Open Plan Health to see whether healthcare creates a weak spot.

- Review Confidence and ending balances.

The goal is to avoid a plan that looks good before healthcare and weak after healthcare.

Healthcare Bridge Checklist

Before retiring before Medicare, answer:

- What date does employer coverage end?

- Do I qualify for a Special Enrollment Period?

- Can I join a spouse's employer plan?

- Is retiree health coverage available?

- Is COBRA available?

- How long would COBRA last?

- What would COBRA cost?

- What Marketplace plans are available in my area?

- What income will I estimate for the coverage year?

- Will IRA or 401k withdrawals count as income?

- Will Roth conversions affect Marketplace savings?

- What happens when Medicare starts?

- What if healthcare costs rise faster than expected?

- What if I need expensive prescriptions?

FAQ

Can I retire before 65 and buy Marketplace coverage?

Yes. HealthCare.gov says if you retire before age 65 and lose job-based health coverage, you can use the Health Insurance Marketplace to buy a plan.

Does losing job-based coverage qualify for a Special Enrollment Period?

HealthCare.gov says yes. Losing job-based coverage can qualify you for a Special Enrollment Period, meaning you may be able to enroll outside the annual Open Enrollment Period.

Do IRA or 401k withdrawals count as income for Marketplace coverage?

HealthCare.gov says generally yes. That is why withdrawal planning matters during pre-Medicare years.

Can I use Marketplace coverage until Medicare starts?

HealthCare.gov says you can get a Marketplace plan to cover you before Medicare begins and then cancel the Marketplace plan once Medicare coverage starts.

Is COBRA always better than Marketplace coverage?

No. COBRA may keep the same group plan for a limited period, but DOL says qualified individuals may have to pay the entire premium, up to 102 percent of plan cost. Compare premiums, deductibles, networks, prescriptions, and timing.

Can I drop COBRA and switch to Marketplace coverage anytime?

Not always. HealthCare.gov says if COBRA runs out outside Open Enrollment, you may qualify for a Special Enrollment Period. But choosing to drop COBRA outside Open Enrollment generally does not create a Special Enrollment Period.

Should I avoid Roth conversions before Medicare?

Not automatically. Roth conversions can help some plans, but they may raise income during Marketplace years. Model the tax and healthcare effects together.

Sources

- HealthCare.gov, Health Coverage For Retirees: https://www.healthcare.gov/retirees/

- HealthCare.gov, Saving Money On Health Insurance: https://www.healthcare.gov/lower-costs/

- Medicare.gov, Prepare To Sign Up: https://www.medicare.gov/basics/get-started-with-medicare/sign-up

- U.S. Department of Labor, Continuation of Health Coverage COBRA: https://www.dol.gov/general/topic/health-plans/cobra