Quick Answer

Yes, you may be able to retire at 60, but age 60 creates a difficult bridge period.

At 60, you are usually:

- Too young for Social Security retirement benefits

- Too young for Medicare

- Close to the age when many retirement account withdrawals become easier

- Old enough that a five-year healthcare and cash-flow plan matters a great deal

- Young enough that your retirement could last 30 years or more

The key question is not only whether you have enough saved. It is whether your plan can cover the years from 60 to 65, then still support the rest of retirement after Social Security, Medicare, RMDs, taxes, inflation, and survivor planning are included.

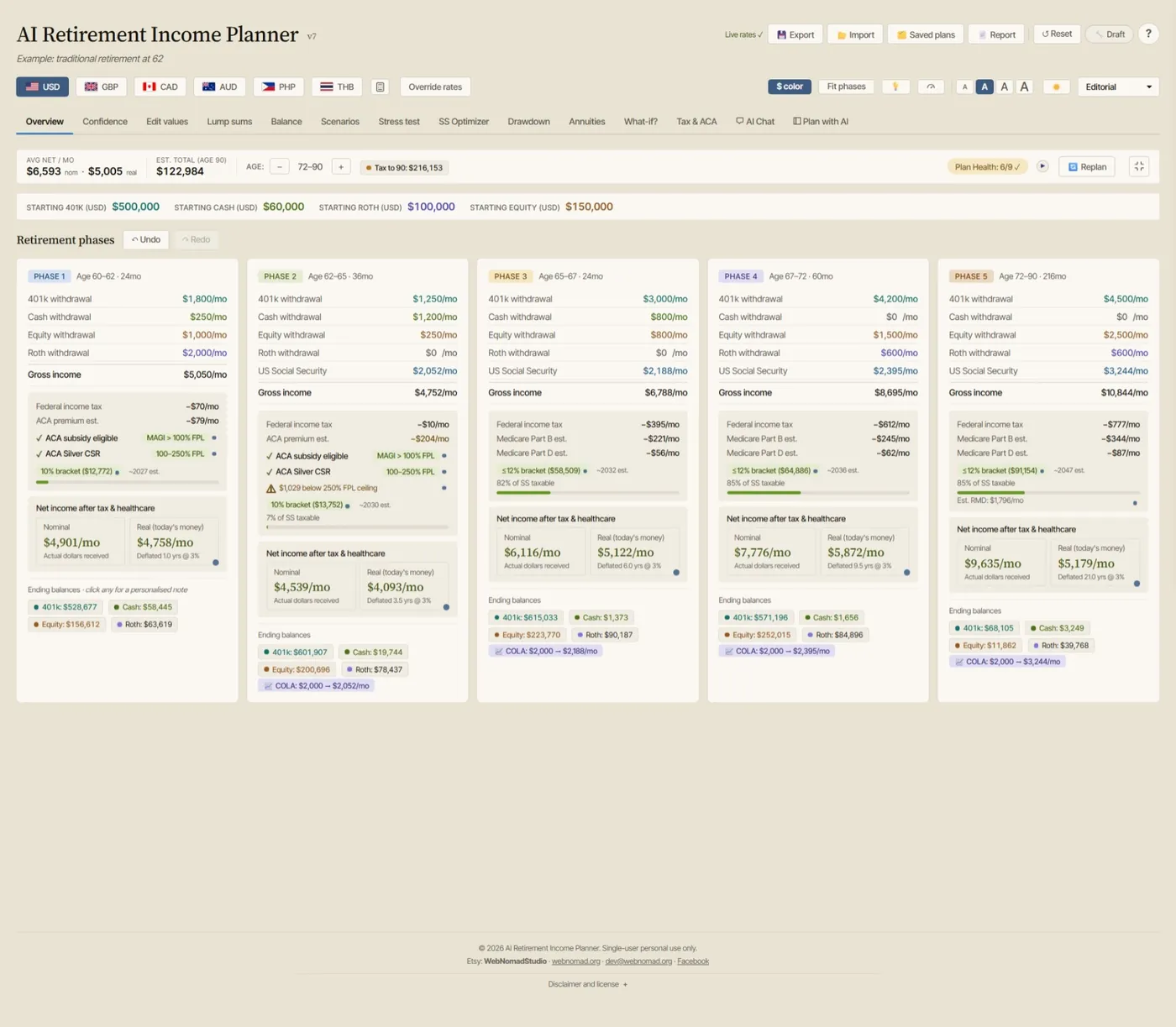

The AI Retirement Income Planner helps by letting you model retirement age, Social Security timing, healthcare, taxes, account withdrawals, Roth conversions, lump sums, stress tests, and scenarios in one private browser-based planner.

Why Age 60 Is A Special Retirement Age

Retiring at 60 feels close to traditional retirement, but it is still early retirement.

The biggest issue is timing. A person retiring at 60 may need to fund several years before major retirement systems begin.

Social Security retirement benefits generally cannot start until age 62. The Social Security Administration says benefits can start as early as age 62, but benefits started before full retirement age are reduced. SSA also notes that if you delay beyond full retirement age up to age 70, the benefit amount increases.

Medicare is usually not available until age 65. SSA's retirement planning guidance says most people will not be covered by Medicare until they reach 65. That means someone retiring at 60 often needs a health insurance bridge.

That five-year gap is where many age-60 plans need the most attention.

The Age 60 Retirement Timeline

An age-60 retirement plan should be built around several key ages.

Age 60

This is the retirement start date in the scenario. Work income may stop. Employer health insurance may stop. Portfolio withdrawals may begin. Spending may rise if travel or lifestyle plans start immediately.

Age 59 1/2

The IRS says withdrawals from an IRA or retirement plan before reaching age 59 1/2 are generally early distributions and may be subject to an additional 10 percent tax unless an exception applies. At age 60, many people are past this threshold, but account type and plan rules still matter.

Age 62

This is generally the earliest age for Social Security retirement benefits. Claiming at 62 can help cash flow, but it usually means a reduced monthly benefit compared with full retirement age.

Age 65

This is the usual Medicare age. If you retire at 60, you may need about five years of non-Medicare health coverage.

Full Retirement Age

Full retirement age depends on birth year. Claiming before full retirement age generally reduces benefits. Claiming at full retirement age or later can increase the monthly amount compared with early claiming.

Age 70

Delaying Social Security beyond full retirement age can increase the benefit up to age 70. That can help later-life income, but it may require larger withdrawals between 60 and 70.

In the planner, these ages can be tested together. The goal is to see whether the bridge years are affordable without weakening the later years too much.

The Five-Year Healthcare Bridge

Healthcare is often the biggest practical issue when retiring at 60.

If you lose job-based health coverage, HealthCare.gov says retirees before age 65 without health coverage may use the Health Insurance Marketplace to buy a plan. Losing job-based coverage can qualify someone for a Special Enrollment Period. Marketplace applications can also show whether someone qualifies for premium tax credits and lower out-of-pocket costs based on income and household size.

Possible healthcare bridge options include:

- Marketplace coverage

- COBRA

- Retiree health benefits

- A spouse's employer plan

- Private insurance

- Part-time work with benefits

- Health savings account funds, if available

The planning issue is that healthcare costs may depend on taxable income. IRA withdrawals, Roth conversions, taxable investment gains, pension income, part-time work, and Social Security can all affect income.

This is why retiring at 60 should be modeled with healthcare and taxes together, not in separate spreadsheets.

Social Security At 62 Or Later

Retiring at 60 does not mean you have to claim Social Security at 62.

You have several broad choices:

- Claim at 62 to reduce portfolio withdrawals earlier

- Claim at full retirement age for a higher monthly benefit

- Delay toward 70 for a larger benefit

- Use one spouse's benefit earlier and delay the other, if appropriate

- Coordinate survivor benefit planning for a married couple

SSA explains that there is no best age for everyone and that the monthly benefit amount can differ greatly based on when benefits start. If benefits begin before full retirement age, the benefit is smaller but paid for a longer period. If benefits start at full retirement age or later, the monthly benefit is larger but paid for a shorter period.

For age-60 retirees, the tradeoff is clear. Delaying Social Security may strengthen later income, but the household must fund the gap from savings or other income.

The planner's Social Security Optimizer can help compare these claiming ages inside the full plan.

Account Withdrawals At Age 60

At 60, many retirees can access traditional retirement accounts without the same early distribution concern that applies before age 59 1/2. But account withdrawals still need planning.

Important issues include:

- Traditional IRA and 401k withdrawals may be taxable

- Roth withdrawals have their own rules

- Taxable brokerage withdrawals may create capital gains

- Cash can reduce the need to sell investments during a downturn

- Large withdrawals can affect ACA subsidies before Medicare

- Later RMDs may affect taxes and Medicare IRMAA

- Withdrawal order can affect survivor planning

The IRS early distribution rules matter most if someone retires before 59 1/2 or has account-specific restrictions. IRS guidance lists several exceptions to the additional tax, including distributions after age 59 1/2, certain substantially equal periodic payments, and a separation-from-service exception for some qualified plans when the employee separates during or after the year they reach age 55. These rules are technical, so this is an area to confirm with a tax professional.

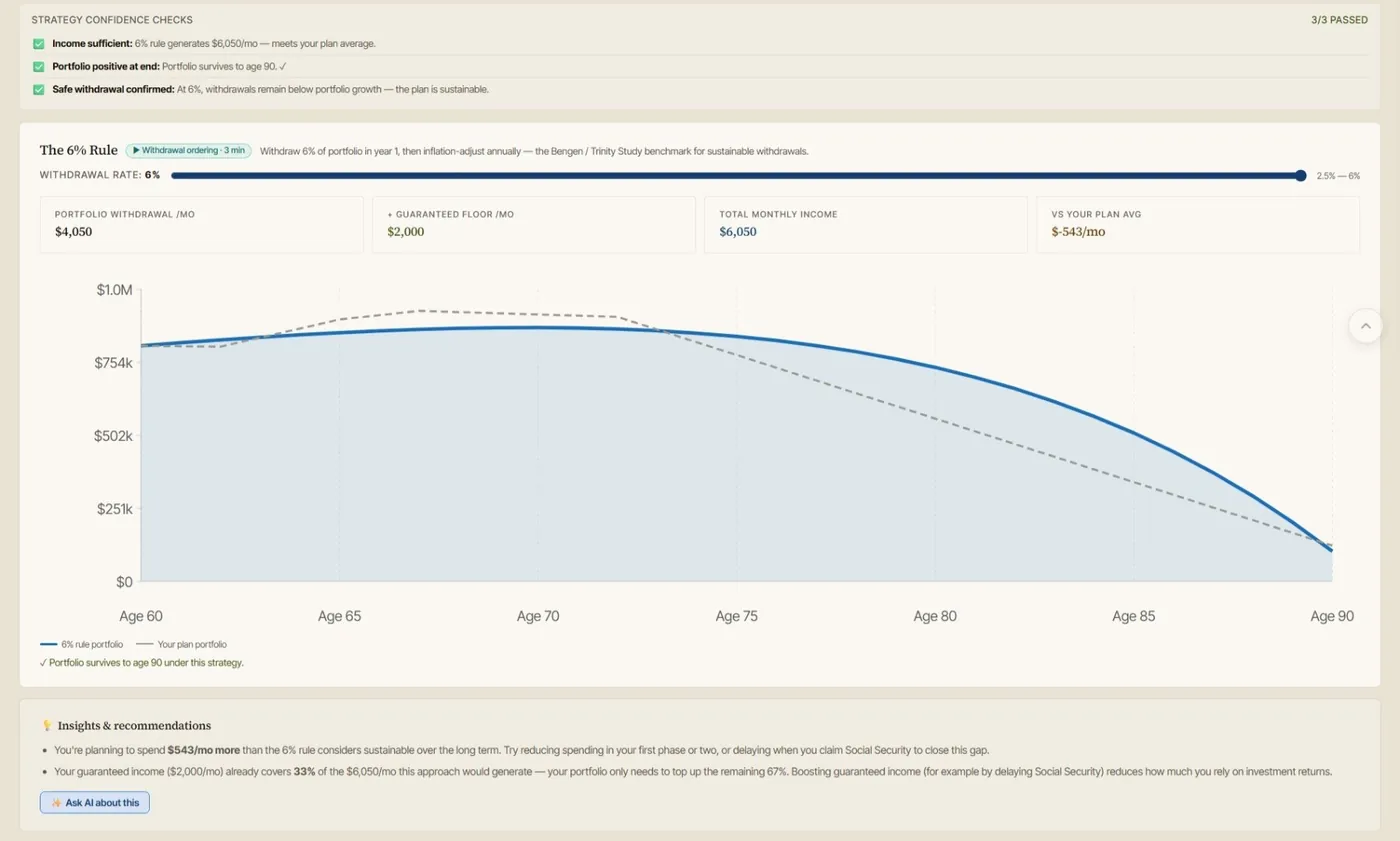

In the planner, the Edit values, Tax & ACA, Balance, and Scenarios tabs can help test withdrawal order, while the Drawdown tab compares withdrawal-rate strategies.

The Big Questions Before Retiring At 60

Before retiring at 60, answer these questions:

- How much will you spend each year from 60 to 65?

- How will you pay for health insurance before Medicare?

- What taxable income will your healthcare plan use?

- Will you claim Social Security at 62 or delay?

- How much will you withdraw before Social Security starts?

- Which accounts will you spend from first?

- How much cash will you keep?

- What happens if the market falls in the first five years?

- What happens if inflation is higher than expected?

- What happens if you or your spouse live into your 90s?

- How will RMDs affect later taxes?

- What happens to the surviving spouse?

- Can you reduce spending if the plan weakens?

- Would part-time work for one or two years improve the result?

- What would make you postpone retirement?

If several answers are unclear, the age-60 plan needs more work.

A Sample Age 60 Retirement Scenario

Assume a married couple is age 60 and 58. The older spouse wants to retire now. The younger spouse may work two more years.

They have:

- $100,000 in cash

- $300,000 in taxable investments

- $850,000 in traditional retirement accounts

- $175,000 in Roth accounts

- No pension

- Estimated Social Security benefits available starting at 62

- Desired spending of $95,000 per year before taxes and healthcare

- Marketplace coverage needed until Medicare

- A $40,000 vehicle purchase planned in three years

- A goal to travel heavily for the first four years

The base case question is: can they retire now?

A better set of questions is:

- Can they cover health insurance from 60 to 65?

- Does the younger spouse's work income help preserve ACA subsidies or hurt them?

- Should Social Security start at 62, full retirement age, or later?

- Would spending more cash early reduce taxable income?

- Would Roth conversions help later RMDs or create healthcare cost problems now?

- What happens if the market drops during the first three retirement years?

- Does the surviving spouse still have enough income?

In the AI Retirement Income Planner, they could create several scenarios:

- Retire at 60, claim Social Security at 62

- Retire at 60, delay Social Security to full retirement age

- Work one more year

- Work part time for two years

- Reduce early travel spending

- Use different withdrawal orders

The answer comes from comparing those scenarios.

How Much Should You Have Saved To Retire At 60?

There is no single savings number that guarantees retirement at 60.

The needed amount depends on:

- Annual spending

- Healthcare costs before Medicare

- Social Security estimates

- Pension or annuity income

- Account types

- Tax rates

- Investment return assumptions

- Inflation assumptions

- Mortgage or debt

- Family support

- Location

- Longevity

- Flexibility

A person with $900,000 saved, low spending, a paid-off home, and a spouse with health insurance may be in better shape than someone with $1.5 million saved, high spending, no healthcare bridge, and large taxable withdrawals.

The planner is useful because it does not treat savings as one pile. It separates account types, timing, taxes, healthcare, spending, and income sources.

Spending Flexibility Matters More At 60

Retiring at 60 often means more retirement years to fund. That makes flexibility valuable.

Helpful forms of flexibility include:

- Reducing travel after a bad market year

- Keeping part-time income available

- Delaying a large purchase

- Using cash during market declines

- Adjusting Roth conversion amounts

- Moving Social Security timing

- Downsizing if needed

- Reducing gifts temporarily

- Choosing a lower-cost health plan if appropriate

Flexibility can make the difference between a plan that fails under stress and a plan that can adapt.

Taxes From 60 To 73 And Beyond

The tax pattern can shift several times after retiring at 60.

Possible phases:

- Age 60 to 61: portfolio withdrawals before Social Security

- Age 62 to 64: possible Social Security plus pre-Medicare healthcare

- Age 65 to RMD age: Medicare begins, but RMDs may not yet apply

- RMD years: required distributions may increase taxable income

- Survivor years: filing status and income sources may change

This is why the first five years should not be planned in isolation. A tax move that helps at 60 might create problems at 65. A Roth conversion that helps at 75 might raise healthcare costs at 61.

Stress Tests For Retiring At 60

An age-60 plan should be stress tested because the first decade matters.

Run these tests:

- Market decline during the first three years

- Lower long-term returns

- Higher healthcare costs before Medicare

- Higher general inflation

- Higher healthcare inflation

- Social Security claimed earlier

- Social Security delayed

- One spouse dies early

- One spouse lives to 95 or 100

- Travel spending stays high longer than expected

- Home repair or vehicle replacement arrives early

- Part-time work income does not happen

If the plan only works in the best case, retiring at 60 may be too fragile. If it still works under reasonable stress tests, the decision becomes more credible.

How The AI Retirement Income Planner Helps With Age 60 Retirement

The AI Retirement Income Planner can help you test an age-60 retirement in one place.

A practical workflow:

- Enter current age, spouse age, retirement age, and life expectancy assumptions.

- Add current account balances by type.

- Add desired spending and special expenses.

- Enter healthcare assumptions for the years before Medicare.

- Add Social Security estimates.

- Compare Social Security claiming ages.

- Review taxes and ACA-related effects.

- Review account drawdown order.

- Add known lump sum expenses.

- Run stress tests.

- Check Confidence and Plan Health.

- Save multiple Scenarios.

- Use the Report button to document the plan.

The goal is not to force one answer. The goal is to make the tradeoffs visible.

FAQ

Can I retire at 60 with $1 million?

Maybe. It depends on spending, healthcare costs, Social Security timing, taxes, account types, investment returns, inflation, debt, and how long retirement lasts. A $1 million portfolio can support very different lifestyles depending on the household.

Can I get Social Security at 60?

Social Security retirement benefits generally cannot start at 60. SSA says retirement benefits can start as early as age 62, but benefits started before full retirement age are reduced.

Can I get Medicare at 60?

Most people are not eligible for Medicare at 60. SSA notes that most people will not be covered by Medicare until age 65. Some people may qualify earlier due to disability or specific conditions, but that is not the usual retiree path.

What health insurance can I use if I retire at 60?

Possible options include Marketplace coverage, COBRA, retiree health coverage, a spouse's employer plan, private insurance, or part-time work with benefits. HealthCare.gov says retirees before 65 who lose job-based coverage may use the Marketplace to buy a plan.

Is it better to claim Social Security at 62 if I retire at 60?

Not always. Claiming at 62 can reduce early portfolio withdrawals, but it also usually reduces the monthly benefit compared with full retirement age or delayed claiming. Couples should also consider survivor income.

Do I pay a penalty on retirement account withdrawals at 60?

Many early distribution concerns apply before age 59 1/2. The IRS says early withdrawals before age 59 1/2 may be subject to an additional 10 percent tax unless an exception applies. Taxes may still apply to traditional retirement account withdrawals at 60.

Should I work part time if I retire at 60?

Part-time work can help bridge the years before Social Security and Medicare. It can reduce withdrawals and may provide health coverage, but it can also affect taxes and ACA subsidy calculations.

What is the biggest risk of retiring at 60?

The biggest risk is often the combination of early withdrawals, healthcare before Medicare, and market losses early in retirement. A plan should test all three together.

Suggested Product CTA

Thinking about retiring at 60? The AI Retirement Income Planner lets you model the bridge years before Medicare and Social Security, compare claiming ages, test healthcare and taxes, and save multiple retirement scenarios privately in your browser.

Sources And References

- Social Security Administration, "Starting Your Retirement Benefits Early": https://www.ssa.gov/benefits/retirement/planner/agereduction.html

- Social Security Administration, "What Important Things to Consider When Planning for Retirement": https://www.ssa.gov/benefits/retirement/planner/otherthings.html

- HealthCare.gov, "Health coverage for retirees": https://www.healthcare.gov/retirees/

- Internal Revenue Service, "Retirement topics - Exceptions to tax on early distributions": https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-exceptions-to-tax-on-early-distributions