Quick Answer

The amount you can spend in retirement depends on your guaranteed income, portfolio size, taxes, healthcare costs, inflation, Social Security timing, life expectancy, withdrawal order, market returns, and flexibility.

A useful starting formula is:

Retirement spending capacity = reliable income + sustainable withdrawals - taxes - healthcare costs - reserves for irregular expenses

That formula is more useful than asking for one universal percentage. A household with a pension, low fixed costs, and flexible travel spending can often spend differently than a household that relies heavily on investments, retires before Medicare, and has large taxable withdrawals.

The AI Retirement Income Planner helps by letting you enter spending, income, Social Security, pensions, healthcare, taxes, accounts, lump sums, and scenarios. Then you can test whether the spending level still works when assumptions change.

Why This Question Is Hard

"How much can I spend in retirement?" sounds simple.

It is not simple because spending is connected to almost everything else in the plan:

- When you retire

- When Social Security begins

- Whether you have a pension

- How much is in taxable, tax-deferred, Roth, and cash accounts

- Whether you retire before Medicare

- How much taxable income you create each year

- Whether RMDs will raise future income

- How your investments perform early in retirement

- Whether inflation runs higher than expected

- How long you and your spouse live

- Whether spending is flexible

Two households can both have $1 million saved and still have very different spending limits.

One household may have two Social Security benefits, a pension, no mortgage, and modest travel plans. Another may have no pension, a mortgage, high healthcare costs, and plans to retire at 60. The same portfolio balance does not produce the same answer.

That is why a retirement spending plan should be built from cash flow, taxes, and risk testing, not from one shortcut.

Start With Spending Categories

The first step is to separate spending into categories. A single annual number is too blunt.

Use at least these groups:

- Essential household spending

- Housing costs

- Property taxes and insurance

- Food and utilities

- Transportation

- Healthcare premiums

- Out-of-pocket healthcare costs

- Travel

- Hobbies and gifts

- Home repairs

- Vehicle replacement

- Taxes

- Emergency reserve

- One-time expenses

Some expenses continue for life. Some fade after the early retirement years. Some increase faster than normal inflation. Some happen once.

For example, a couple might plan to spend $110,000 per year during the first five retirement years because they want to travel. Later, they may expect spending to fall to $88,000. Healthcare may rise faster than general spending. A vehicle purchase may happen every seven years. A home repair may happen in one specific year.

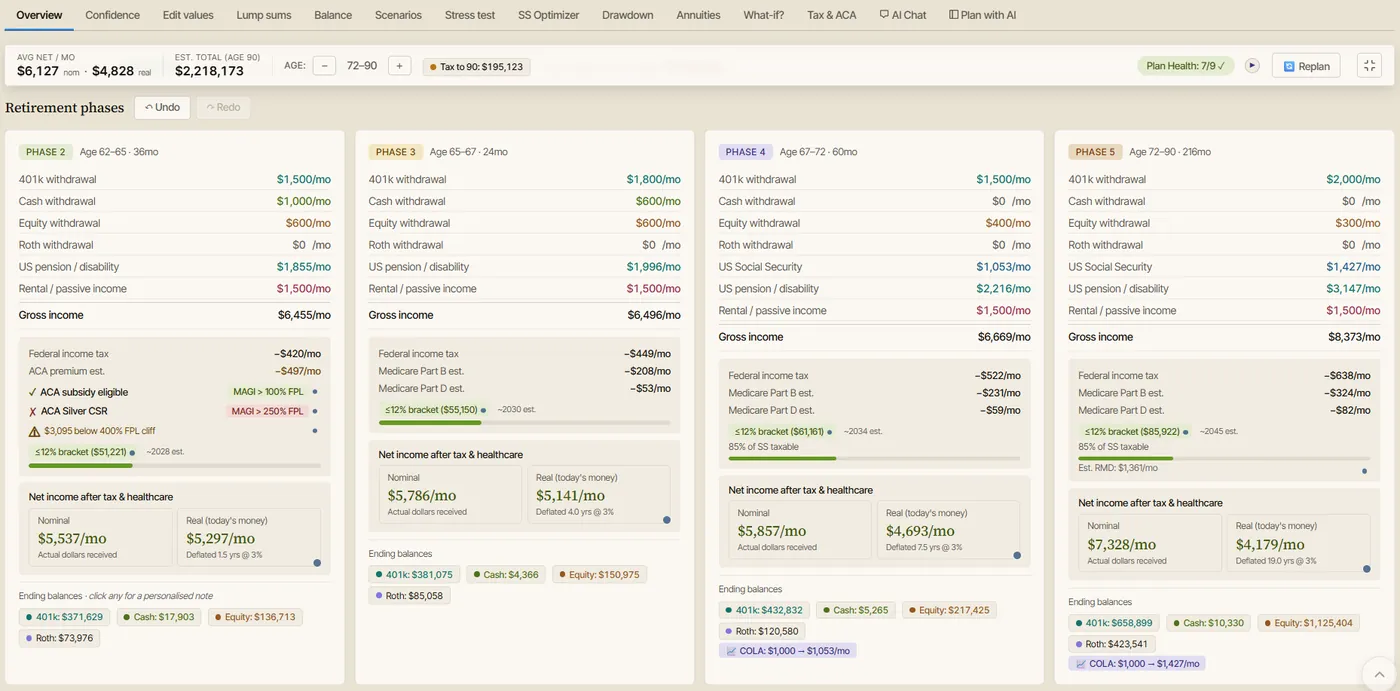

The planner can handle those differences better than a flat spending number because it supports ongoing expenses, special spending, inflation assumptions, healthcare assumptions, and lump sum events.

Separate Gross Spending From Spendable Income

A common mistake is comparing retirement spending to gross retirement income.

If you want to spend $85,000 per year on living expenses, you may need more than $85,000 of gross income or withdrawals because taxes and healthcare costs may come out first.

For retirement planning, separate these numbers:

- Gross income: Social Security, pension, work income, annuity income, rental income, withdrawals

- Taxes: federal income tax, state income tax where relevant, capital gains tax, tax on Social Security, tax on IRA withdrawals

- Healthcare: insurance premiums, Medicare premiums, out-of-pocket costs, prescriptions, dental, vision, long-term care planning if relevant

- Net lifestyle spending: the amount available for household spending after taxes and healthcare

The useful question is not "Can I withdraw $90,000?"

The useful question is "After taxes and healthcare, can this plan support the spending I actually need?"

A Practical Retirement Spending Method

Here is a practical way to estimate how much you can spend.

Step 1: Estimate Essential Spending

Start with the spending that must be paid even in a bad year:

- Housing

- Utilities

- Groceries

- Insurance

- Basic transportation

- Healthcare

- Debt payments

- Taxes

This number tells you how much income security you need.

If Social Security, pensions, annuities, and other reliable income cover most essential costs, the plan may have more flexibility. If essential costs depend heavily on portfolio withdrawals, the plan may need more caution.

Step 2: Estimate Lifestyle Spending

Next, list the spending that could be adjusted if needed:

- Travel

- Dining out

- Hobbies

- Gifts

- Home projects

- New vehicles

- Seasonal living

- Large discretionary purchases

Flexible spending is valuable. A household that can reduce travel after a bad market year may be able to accept more portfolio risk than a household with fixed spending.

Step 3: Add Irregular Spending

Retirement spending rarely moves in a straight line.

Add known irregular costs:

- Roof replacement

- Vehicle purchases

- Major dental work

- Relocation

- Home accessibility updates

- Family support

- Large anniversaries or trips

- College help for grandchildren

- Long-term care planning costs

The planner's Lump sums area is useful for this because it lets you place one-time expenses in the year they are expected.

Step 4: Add Healthcare

Healthcare needs its own section.

Medicare.gov explains that Medicare costs vary based on coverage, services, and providers. Costs can include premiums, deductibles, coinsurance, copayments, and prescription drug costs. Original Medicare also does not have a yearly out-of-pocket limit unless you have supplemental coverage or join a Medicare Advantage Plan.

If you retire before 65, you also need a pre-Medicare healthcare plan. That may involve Marketplace coverage, COBRA, retiree coverage, a spouse's employer plan, or private insurance.

Do not treat healthcare as a small footnote. It can change both spending and tax planning.

Step 5: Add Taxes

Taxes can change the spending answer.

Traditional IRA and 401k withdrawals are usually taxable. Roth withdrawals may be tax-free if rules are met. Taxable brokerage withdrawals may create capital gains. Social Security may be partly taxable depending on income. RMDs may increase taxable income later.

If you ignore taxes, you may overestimate spending capacity.

The planner's Tax & ACA tab can help show year-by-year tax effects instead of relying on one retirement tax estimate.

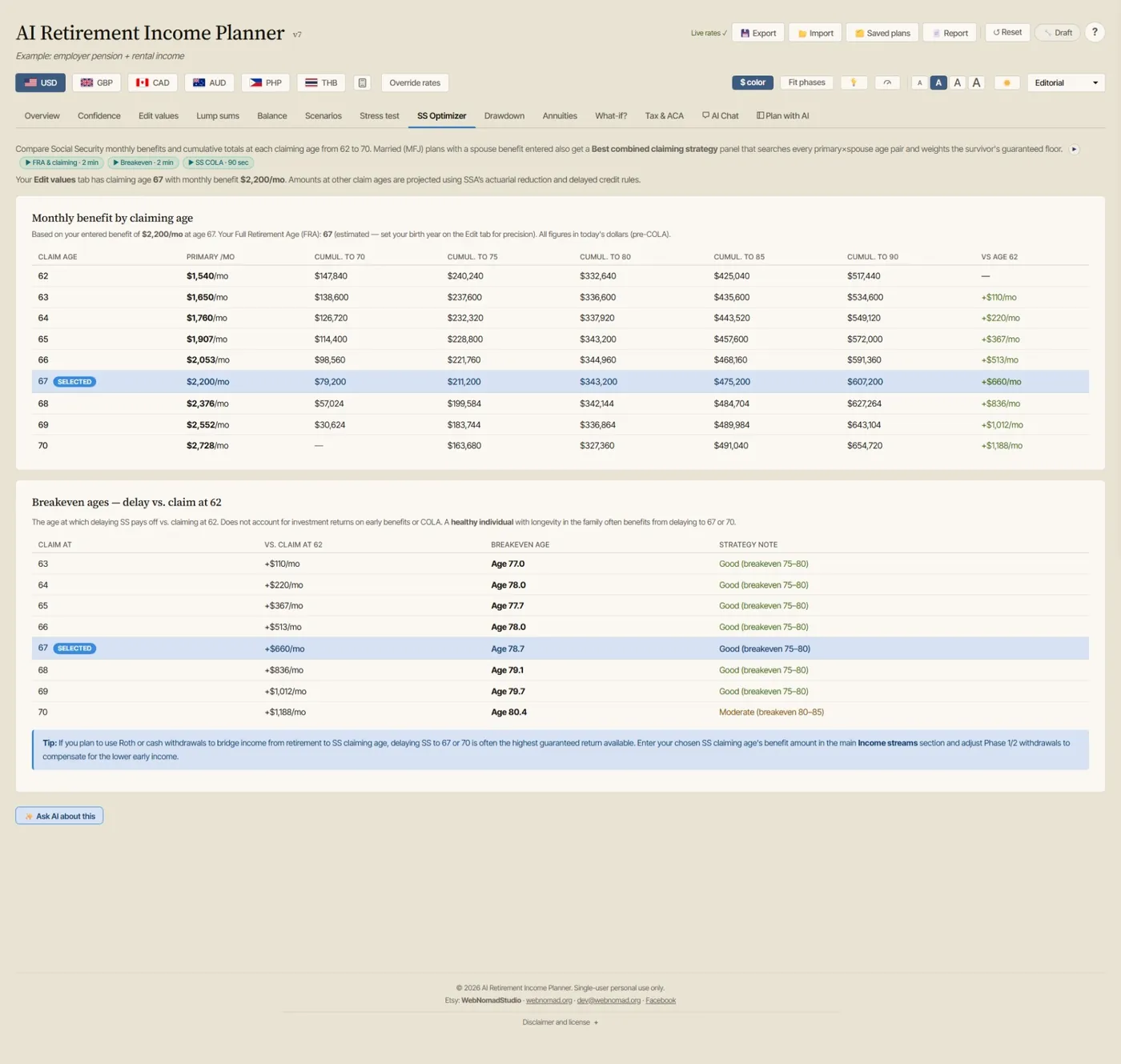

Step 6: Test Social Security Timing

Deciding whether to claim Social Security at 62 or wait can change how much you can spend.

The Social Security Administration says there is no single best age for everyone. Benefits are smaller if started before full retirement age and larger if started at full retirement age or later. SSA also notes that the first benefit amount becomes the base for what you receive for the rest of your life.

Claiming earlier can reduce portfolio withdrawals in the bridge years. Claiming later can raise lifetime guaranteed income, but it may require larger withdrawals before benefits begin.

For couples, Social Security timing also affects survivor income. That makes it part of the spending question, not a separate decision.

Step 7: Include RMDs Before They Begin

Required minimum distributions can change future spending and tax results.

The IRS explains that retirement account owners generally must take minimum distributions each year once RMD rules apply. For retirees with large traditional IRA or 401k balances, RMDs may push taxable income higher later in retirement.

This matters for spending because a plan may look tax-efficient early but become tax-heavy later. It may also create Medicare IRMAA exposure or reduce flexibility.

A spending plan should look past the first few retirement years and include future RMDs.

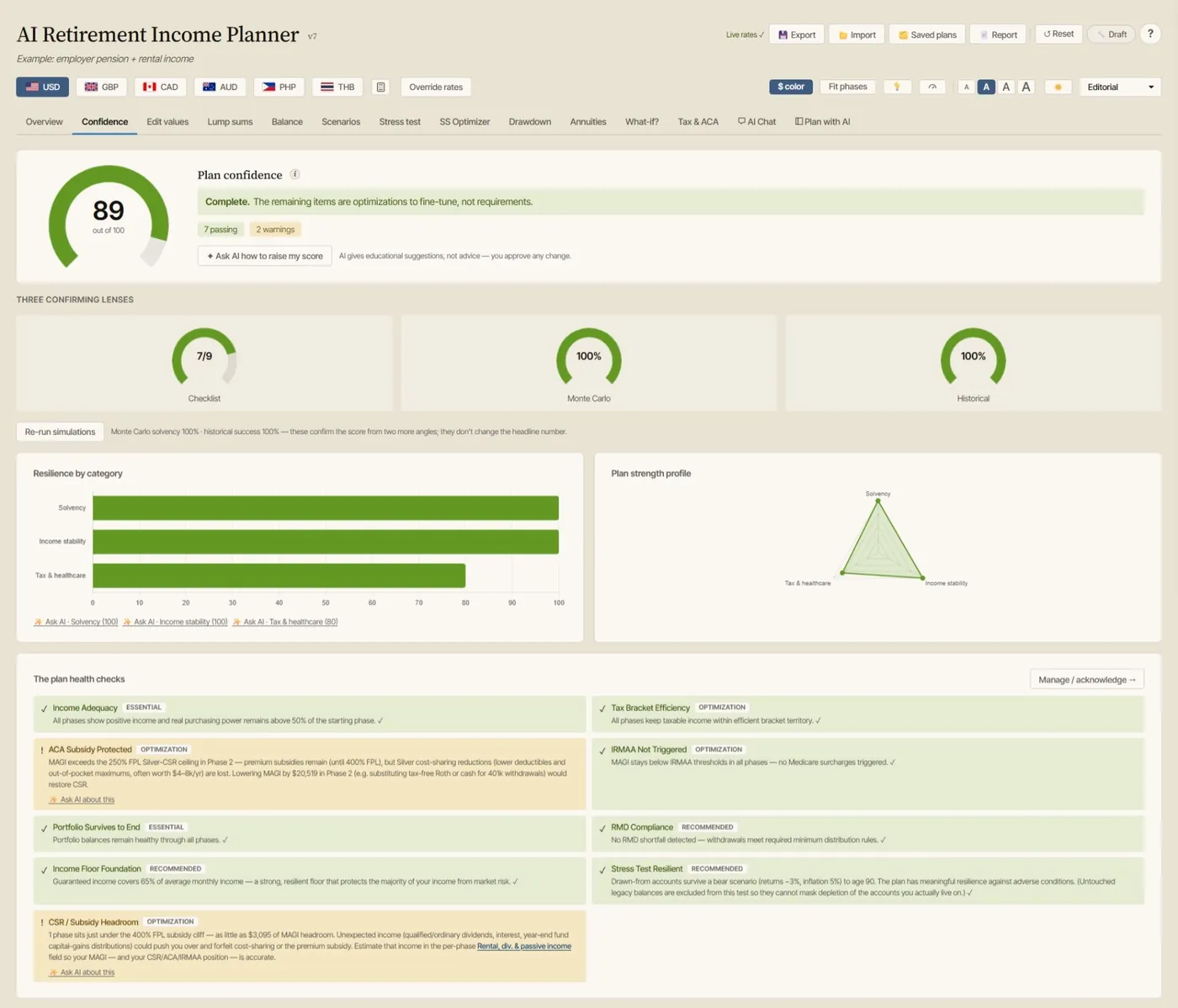

Step 8: Stress Test The Spending Level

Once you have a spending number, test it.

At minimum, test:

- Lower investment returns

- Poor returns in the first 5 to 10 retirement years

- Higher inflation

- Higher healthcare inflation

- Longer life

- Earlier death of one spouse

- Higher taxes

- Delayed home sale or business sale

- One large unexpected expense

Investor.gov explains that investors face different kinds of risk, including volatility risk, inflation risk, and liquidity risk. Retirement spending touches all three. A market decline can reduce balances, inflation can reduce purchasing power, and liquidity problems can make it harder to raise cash when needed.

The planner's Confidence and Stress test tabs are designed for this review. If the plan fails under every modest stress test, the spending level may be too high. If it survives several reasonable stress tests, the number may be more credible.

Why The 4 Percent Rule Is Only A Starting Point

Many people start with the 4 percent rule. In plain language, it suggests that a retiree might withdraw around 4 percent of the starting portfolio in the first retirement year, then adjust withdrawals for inflation.

It can be a useful starting point, but it is not a full spending plan.

It does not automatically account for:

- Taxes

- Medicare costs

- ACA subsidies

- RMDs

- Roth conversions

- Pension income

- Annuities

- Rental income

- Uneven spending

- Early retirement before Medicare

- Large one-time expenses

- Survivor planning

- Social Security claiming age

- Country-specific tax differences

For example, 4 percent of a $1 million portfolio is $40,000 in the first year. But if a household also has $48,000 of Social Security and a pension, spending capacity may be higher than $40,000. If the household has no Social Security yet, high healthcare costs, and large taxes, spendable income may be lower.

The planner lets you use withdrawal rules as one input, then check the full plan around them.

Example: Estimating Retirement Spending

Assume a married couple is 63 and 61. They want to retire when the older spouse turns 64.

They have:

- $120,000 in cash

- $350,000 in taxable investments

- $900,000 in traditional retirement accounts

- $200,000 in Roth accounts

- Estimated Social Security of $3,400 per month if both claim at full retirement age

- No pension

- Desired spending of $92,000 per year before taxes and healthcare

- Planned travel spending of $18,000 per year for the first five years

- Pre-Medicare healthcare costs for one spouse

- A $45,000 vehicle purchase planned in year three

At first, they might ask, "Can we spend $92,000?"

A better review asks:

- What is the real spending number after healthcare is added?

- How much must come from the portfolio before Social Security begins?

- Would claiming Social Security earlier reduce risk or reduce lifetime income too much?

- Would partial Roth conversions help future tax planning?

- How much will RMDs add later?

- What happens if the market drops in the first three years?

- Can travel spending be reduced if needed?

- What happens to the surviving spouse?

In the planner, this couple could create three scenarios:

- Scenario A: Retire at 64 and claim Social Security at full retirement age

- Scenario B: Retire at 64 and delay the higher earner's Social Security to 70

- Scenario C: Work one more year and reduce early travel spending by $8,000 per year

The spending answer comes from comparing the scenarios, not from guessing.

Signs You May Be Spending Too Much

Your retirement spending level may be too high if:

- The plan depends on strong investment returns every year

- Account balances fall quickly in the first decade

- You run out of liquid assets before later income starts

- Healthcare costs are estimated too low

- Taxes are missing from the plan

- RMDs are ignored

- The surviving spouse's plan is weak

- Inflation stress tests fail quickly

- Travel and discretionary spending cannot be reduced

- You need to sell investments during every market decline

- The plan has no emergency reserve

These signs do not mean retirement is impossible. They mean the spending level needs testing.

Signs You May Be Spending Less Than You Could

Some people have the opposite problem. They retire with enough resources but remain afraid to spend.

You may be underspending if:

- Essential expenses are well covered by Social Security, pension, annuity, or other reliable income

- Portfolio balances keep rising under conservative assumptions

- Stress tests still look strong

- RMDs will force taxable withdrawals later anyway

- You have large cash reserves beyond your comfort target

- You have no plan for using money for travel, family, giving, or quality of life

- Survivor outcomes remain strong after reasonable spending increases

The goal is not to spend for the sake of spending. The goal is to make intentional choices.

The planner can help by testing higher spending scenarios as well as lower spending scenarios.

How Much Should Come From Guaranteed Income?

Some retirees want guaranteed income to cover essential expenses. Others are comfortable relying more on investments.

Guaranteed or reliable income may include:

- Social Security

- Pension income

- Income annuities

- Certain rental income, if realistic and net of costs

- Part-time work, if truly dependable

Portfolio withdrawals may cover:

- Discretionary spending

- Travel

- Home projects

- Legacy goals

- Inflation adjustments

- Gaps before Social Security or pensions begin

There is no single correct split. But if essential spending depends heavily on investment withdrawals, the plan should be stress tested carefully.

Retirement Spending Before Medicare

Retiring before Medicare can reduce spending capacity because healthcare must be solved before age 65.

SSA notes that most people are not covered by Medicare until age 65. Medicare.gov also shows that Medicare itself still has premiums and cost sharing after eligibility begins.

A pre-Medicare retiree should model:

- Marketplace premiums

- Possible premium tax credits

- COBRA costs

- Retiree health coverage

- Spouse employer coverage

- Out-of-pocket medical costs

- Dental and vision costs

- The effect of taxable income on ACA subsidies

This is one reason Roth conversions, withdrawals, capital gains, and part-time income should be reviewed together. A move that looks good for taxes may change healthcare costs.

Spending, Inflation, And Longevity

A retirement spending plan has to last for an unknown period.

SSA's retirement planning guidance tells people to plan for the long term and consider life expectancy. Its life expectancy calculator also estimates additional years of life based on sex and date of birth. Averages are useful, but many people live longer than average, especially in married couples where at least one spouse may live into their 90s.

Inflation also matters. If spending starts at $90,000 and rises by 3 percent per year, it is about $121,000 after 10 years and about $163,000 after 20 years. Healthcare may rise differently from general spending.

That is why the spending question should be asked in real dollars and future dollars.

The planner can show spending, balances, and income across a multi-decade retirement instead of only in year one.

Spending Flexibility Is A Planning Asset

Flexibility can make a retirement plan stronger.

Examples:

- Travel more when markets are strong and less after a bad year

- Delay a vehicle purchase

- Reduce gifts temporarily

- Work part time for one more year

- Downsize later if needed

- Use cash reserves during market declines

- Delay a large home project

- Use a guardrail around annual withdrawals

This does not mean you need a bare-bones retirement. It means you know which spending can move if the plan needs help.

In the planner, you can make a base scenario and then create a lower-spending fallback scenario. That makes the fallback plan visible before you need it.

A Retirement Spending Worksheet

Use this worksheet before entering your numbers into a planner:

- Current annual household spending:

- Expenses that will stop after retirement:

- Expenses that will start after retirement:

- Mortgage or rent:

- Property tax and insurance:

- Healthcare before Medicare:

- Medicare premiums and out-of-pocket costs:

- Travel spending:

- Vehicle replacement plan:

- Home repair reserve:

- Gifts and family support:

- Emergency reserve target:

- Expected Social Security:

- Expected pension or annuity income:

- Expected part-time work income:

- Taxable account balance:

- Traditional IRA and 401k balance:

- Roth balance:

- Cash balance:

- Large known future expenses:

- Desired legacy amount:

- Spending that could be reduced in a bad year:

The more precise these inputs are, the more useful the spending estimate becomes.

How The AI Retirement Income Planner Helps Estimate Spending

The AI Retirement Income Planner is useful for spending decisions because it connects the spending number to the rest of the plan.

A practical workflow:

- Enter current ages, retirement ages, life expectancy assumptions, and household details.

- Add Social Security estimates and test claiming ages.

- Add pensions, annuities, rental income, disability income, or part-time work.

- Add account balances by type.

- Enter desired spending and separate special expenses.

- Add healthcare and inflation assumptions.

- Review taxes and ACA or Medicare-related income effects.

- Review account drawdown patterns.

- Run stress tests for market returns, inflation, healthcare, and longevity.

- Check the Confidence tab.

- Open Plan Health to look for warnings.

- Save multiple Scenarios at different spending levels.

- Use the Report button to generate a plan summary.

This turns "Can I spend this much?" into a set of visible tradeoffs.

FAQ

How much can I safely spend in retirement?

There is no single safe amount for everyone. It depends on guaranteed income, savings, taxes, healthcare, inflation, withdrawal order, investment risk, life expectancy, and flexibility. A useful answer requires year-by-year planning and stress testing.

Is 4 percent a good retirement withdrawal rate?

The 4 percent rule can be a starting point, but it is not a complete plan. It may not account for taxes, healthcare, uneven spending, Social Security timing, RMDs, Roth conversions, pensions, annuities, survivor planning, or early retirement before Medicare.

Should I base retirement spending on my current income?

Current income can help, but current spending is usually more useful. Retirement spending should be built from actual expenses, taxes, healthcare, irregular costs, and lifestyle goals.

How do taxes affect retirement spending?

Taxes reduce spendable income. IRA withdrawals, 401k withdrawals, pensions, Social Security taxation, capital gains, and RMDs can all affect the amount available for household spending.

Should healthcare be included in retirement spending?

Yes. Healthcare should be modeled separately because costs can include premiums, deductibles, copayments, coinsurance, prescriptions, dental, vision, and pre-Medicare insurance. Income can also affect ACA subsidies or Medicare IRMAA.

Does Social Security timing affect how much I can spend?

Yes. Claiming earlier can reduce portfolio withdrawals in early retirement, while claiming later can increase monthly income for life. For couples, claiming choices can also affect survivor income.

What if I want to spend more in early retirement?

Many people spend more in the first retirement years on travel or hobbies. That can be reasonable if the plan models higher early spending, lower later spending, taxes, healthcare, and market risk.

How often should I update my retirement spending plan?

Review it at least once per year and after major changes such as retirement, Social Security claiming, a market decline, a health change, a tax law change, a spouse's death, or a major purchase.

Suggested Product CTA

Trying to find a retirement spending number that holds up under taxes, healthcare, Social Security timing, withdrawals, inflation, and stress tests? The AI Retirement Income Planner lets you build and compare private retirement income scenarios in your browser.

Sources And References

- Social Security Administration, "What Important Things to Consider When Planning for Retirement": https://www.ssa.gov/benefits/retirement/planner/otherthings.html

- Social Security Administration, "Life Expectancy Calculator": https://www.ssa.gov/OACT/population/longevity.html

- Medicare.gov, "Costs": https://www.medicare.gov/basics/costs/medicare-costs

- Internal Revenue Service, "Retirement plan and IRA required minimum distributions FAQs": https://www.irs.gov/retirement-plans/retirement-plan-and-ira-required-minimum-distributions-faqs

- Investor.gov, "What is Risk?": https://www.investor.gov/introduction-investing/investing-basics/what-risk