Short Answer

There is no single withdrawal order that works for every retiree.

The familiar rule is to spend taxable accounts first, tax-deferred accounts next, and Roth accounts last. That can be a reasonable starting point, but it can also create problems if it leaves a large traditional IRA or 401k balance to produce bigger RMDs later.

A better question is:

Which withdrawal order gives your household the strongest after-tax income plan across early retirement, RMD years, Medicare years, and survivor years?

Why Withdrawal Order Matters

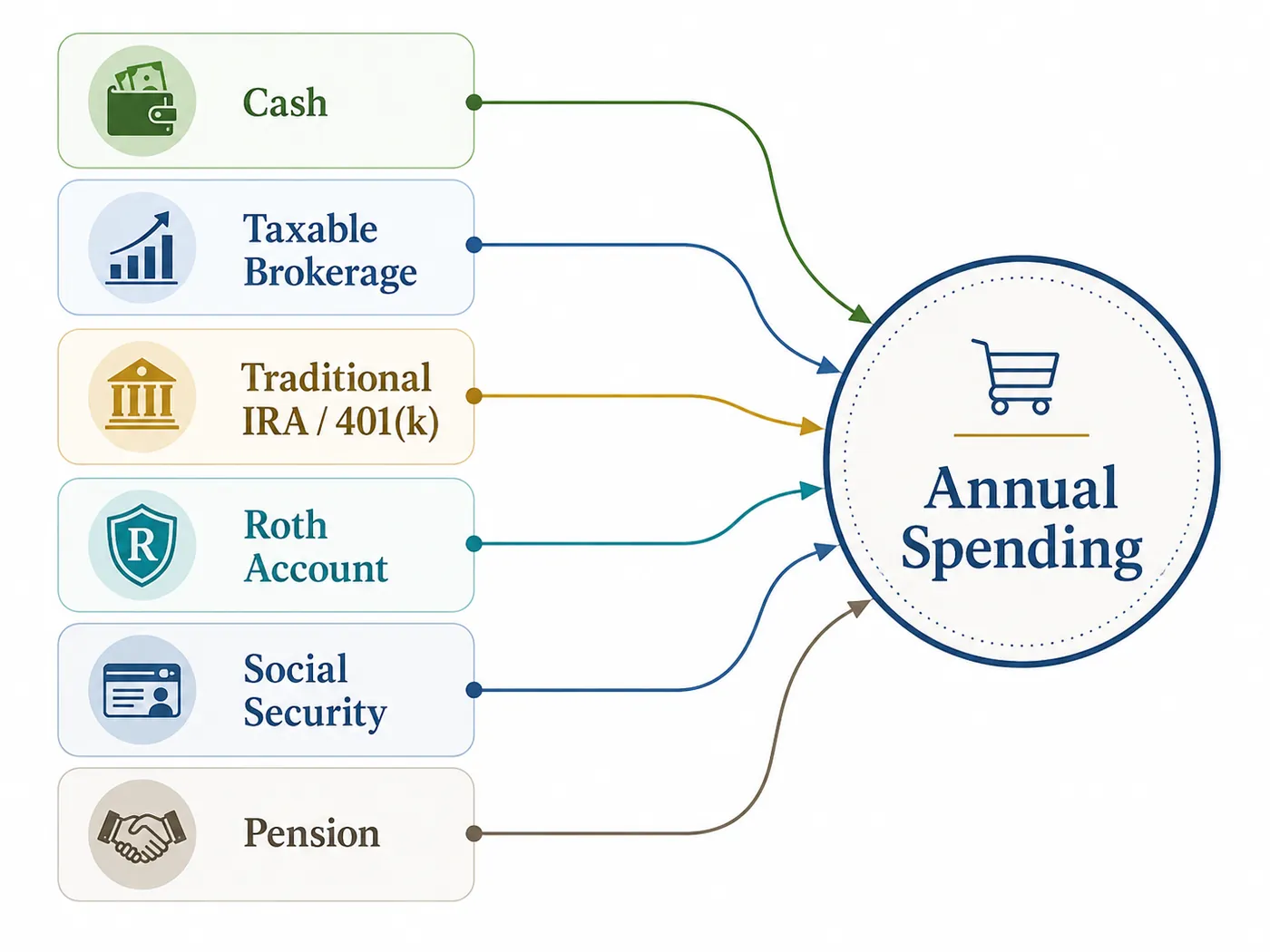

In retirement, the same spending amount can produce different tax results depending on where the money comes from.

For example:

- Cash withdrawals may not create taxable income.

- Selling investments in a taxable account can create capital gains or losses.

- Traditional IRA withdrawals are often taxable.

- 401k withdrawals are often taxable.

- Qualified Roth withdrawals may be tax-free.

- Social Security may become partly taxable when other income is higher.

- RMDs can force taxable withdrawals later.

That is why a withdrawal order is more than a cash-flow schedule. It is a tax, healthcare, risk, and longevity decision.

The Classic Withdrawal Order

The classic order often looks like this:

- Spend cash and taxable accounts.

- Use tax-deferred accounts such as traditional IRAs and 401ks.

- Save Roth accounts for later.

This can work because taxable accounts may have favorable capital gains treatment, while Roth assets may be valuable later in retirement or for heirs.

But the classic order can fail when it ignores the future.

If a retiree avoids traditional IRA withdrawals for too long, the account may grow into a larger RMD problem. The IRS says RMDs generally begin at age 73 for traditional IRAs, SEP IRAs, SIMPLE IRAs, and many retirement plan accounts. Those withdrawals are generally included in taxable income, except for already-taxed basis or tax-free qualified Roth distributions.

That means avoiding IRA withdrawals today can increase taxable income later.

How Different Account Types Behave

Cash

Cash can be useful for near-term spending, emergency needs, and avoiding forced sales during market downturns.

Spending cash usually does not create taxable income. The tradeoff is that too much cash can reduce long-term growth.

Taxable Brokerage

Taxable brokerage accounts are flexible. They do not have retirement-account withdrawal rules, but selling investments can create capital gains or losses.

The IRS says when you sell a capital asset, the difference between your adjusted basis and the amount realized is a capital gain or loss. The IRS also says long-term and short-term gains are treated differently, and net capital gains may be taxed at lower rates than ordinary income.

This makes taxable accounts useful, but they still need planning. A large sale can raise taxable income, affect Social Security taxation, or influence Medicare IRMAA.

Traditional IRA And 401k

Traditional IRA and many 401k withdrawals are often taxable.

The IRS says traditional IRA distributions are fully or partially taxable in the year of distribution. If only deductible contributions were made, distributions are fully taxable.

These accounts can be useful for filling lower-income years before Social Security, pensions, or RMDs begin. They can also create tax pressure later if left untouched for too long.

Roth Accounts

Roth accounts can be especially valuable because qualified distributions may be tax-free.

The IRS says Roth IRA contributions are not deductible, returns of Roth contributions are not subject to tax, and earnings on qualified distributions can also be tax-free. Roth rules have details, including age and five-year requirements, so do not treat every Roth withdrawal as automatically tax-free without checking your situation.

Roth money can be useful for:

- Late-retirement spending

- Large one-time expenses

- Survivor planning

- Managing taxable income

- Reducing pressure in high-tax years

The Tax Bracket Trap

Some retirees try to minimize taxes every single year. That sounds sensible, but it can produce a higher lifetime tax bill.

Example:

A retiree has low taxable income from age 62 to 69 because they delayed Social Security and have no pension yet. They spend only cash and taxable savings to keep taxes low.

At age 70, Social Security begins. At age 73, RMDs begin. Later, the tax return includes Social Security, RMDs, investment income, and possibly pension income.

The early low-tax years were real. The later tax pressure is also real.

Sometimes it is better to pay some tax earlier by using traditional IRA withdrawals or Roth conversions before RMDs begin.

Social Security Changes The Math

Social Security timing can change the withdrawal order.

If you delay Social Security, you may need to draw more from savings before benefits begin. That can feel uncomfortable, but it may also create tax-planning room.

The IRS says Social Security benefits may be taxable when modified adjusted gross income plus one half of Social Security benefits is more than the base amount for your filing status.

That means IRA withdrawals, capital gains, pensions, and other income can affect how much of Social Security is taxable.

Withdrawal order and claiming age should be tested together. See should you claim Social Security at 62 or wait? for that side of the decision.

Medicare IRMAA Changes The Math Too

Medicare income-related premium adjustments can also affect withdrawal planning.

A large IRA withdrawal, Roth conversion, capital gain, or RMD can raise income in a Medicare year. That may affect Part B or Part D premiums for higher-income retirees.

This does not mean you should avoid every higher-income year. It means Medicare costs belong in the comparison. A retirement calculator with taxes and healthcare keeps those costs in view.

A Better Way To Think About Withdrawal Order

Instead of asking which account to spend first, compare phases.

Phase 1: Before Social Security And Medicare

This phase may include:

- Cash spending

- Taxable account sales

- Planned IRA withdrawals

- Roth conversions

- ACA Marketplace income planning

The risk is creating too much income for healthcare subsidies or spending down the wrong accounts too quickly. (Health insurance before Medicare explains that subsidy sensitivity.)

Phase 2: Medicare Before RMDs

This phase may include:

- Medicare premiums

- Social Security timing

- More Roth conversion testing

- Planned traditional IRA withdrawals

- Capital gains planning

The risk is missing useful lower-income years before RMDs begin.

Phase 3: RMD Years

This phase may include:

- Required withdrawals

- Social Security

- Pension income

- Medicare IRMAA exposure

- Survivor planning

The risk is discovering too late that the traditional IRA balance has become the main driver of taxable income.

Phase 4: Survivor Years

For couples, the surviving spouse may have lower household income but a less favorable tax filing status. Some expenses may fall, but many do not fall by half.

The withdrawal order should be tested for both spouses living and for one spouse surviving.

Common Withdrawal Strategies To Compare

Taxable First

Spend cash and taxable investments before traditional IRA or Roth assets.

Potential benefit:

- Keeps tax-deferred and Roth assets invested longer.

Potential risk:

- Can leave larger RMDs later.

IRA Earlier

Use traditional IRA or 401k withdrawals earlier in retirement, especially in lower-income years.

Potential benefit:

- May reduce future RMD pressure.

Potential risk:

- Raises current taxable income.

Roth Last

Preserve Roth assets for later years.

Potential benefit:

- Gives flexibility in high-tax years and survivor years.

Potential risk:

- May force too much taxable income from other accounts earlier.

Proportional Withdrawals

Take some money from multiple account types each year.

Potential benefit:

- Can smooth taxes and preserve flexibility.

Potential risk:

- May be less tax-efficient than a more targeted strategy.

Guardrail Strategy

Change withdrawal sources based on market performance, tax room, and account balances.

Potential benefit:

- More responsive to real conditions.

Potential risk:

- Requires more monitoring.

How To Model Withdrawal Order In The Planner

Use this workflow in the AI Retirement Income Planner:

- Enter household ages, retirement dates, Social Security timing, pensions, healthcare assumptions, spending goals, and account balances.

- Confirm account types in Edit values, including cash, taxable equity, Roth, and tax-deferred accounts.

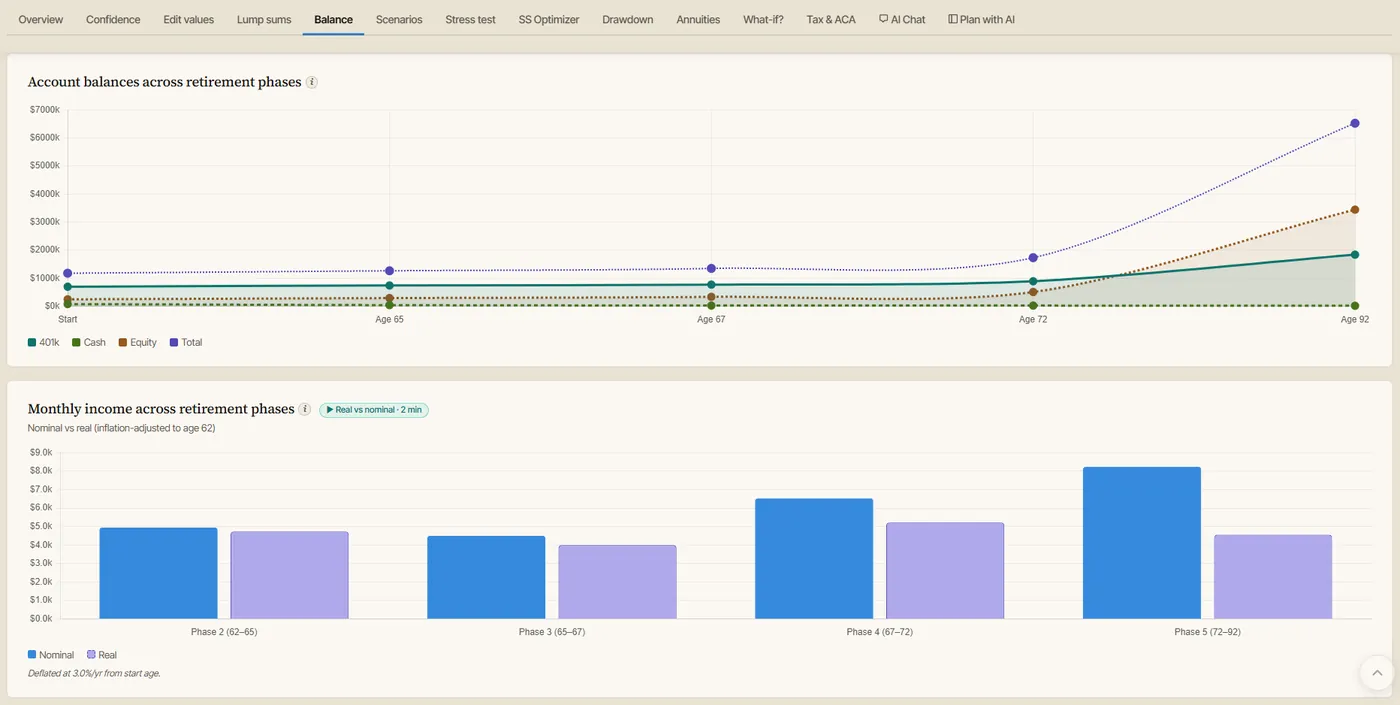

- Set how much each account funds spending in each phase using the phase withdrawal fields (this per-phase mix is your withdrawal order), and use the Drawdown tab to compare withdrawal-rate methods such as the 4% Rule, Guardrails, and bucket strategies.

- Check Balance to see which accounts are being depleted.

- Review Tax & ACA for taxable income, healthcare, and Medicare-sensitive years.

- Use What-if? to test Roth conversions and planned IRA withdrawals.

- Use Scenarios to compare taxable-first, IRA-earlier, Roth-last, and blended approaches.

- Run Stress test to see how strategies behave in weak markets or high inflation. Monte Carlo and historical backtesting add probability and past-market views.

- Open Plan Health to look for warnings.

- Review Confidence and ending balances.

The goal is to compare tradeoffs, not to crown one account as always first.

A Simple Example

Suppose a couple retires at 62 with:

- Cash savings

- A taxable brokerage account

- A traditional IRA

- A Roth IRA

- Social Security planned at 70

- No pension

One strategy spends cash and taxable accounts first. Taxes are low early, but the traditional IRA keeps growing. Later, RMDs begin and taxable income rises.

Another strategy uses planned traditional IRA withdrawals from 62 to 69. Taxes are higher earlier, but future RMDs may be lower.

A third strategy uses partial Roth conversions during lower-income years, then preserves the Roth for later.

The right answer depends on:

- Tax brackets

- ACA or Medicare costs

- Investment returns

- Life expectancy

- Survivor planning

- How much cash the couple wants to keep

- Whether they value lower taxes now or more flexibility later

Questions To Ask Before Choosing A Withdrawal Order

- Which accounts are taxable, tax-deferred, and Roth?

- How much cash do I need for near-term spending?

- When will Social Security begin?

- Will I have pension income?

- Will I use ACA coverage before Medicare?

- Could withdrawals affect Medicare IRMAA?

- What will my RMDs look like after age 73?

- Do I have low-income years before RMDs?

- Should I test Roth conversions?

- What happens if markets fall early in retirement?

- What happens if one spouse dies first?

- Do I care more about lower taxes this year or lower lifetime taxes?

FAQ

Should retirees always spend taxable accounts first?

No. Taxable-first can work for some retirees, but it can also leave larger tax-deferred balances that create bigger RMDs later. Model it against other strategies.

Are traditional IRA withdrawals taxable?

Often, yes. The IRS says traditional IRA distributions are fully or partially taxable in the year of distribution. If only deductible contributions were made, distributions are fully taxable.

Are Roth IRA withdrawals tax-free?

Some Roth withdrawals are tax-free, but the rules matter. The IRS says returns of Roth IRA contributions are not subject to tax, and earnings on qualified distributions can also be tax-free. Nonqualified distributions can be taxable.

Do RMDs affect withdrawal order?

Yes. RMDs can force taxable withdrawals later. The IRS says RMDs generally begin at age 73 for many traditional retirement accounts.

Can withdrawals affect Social Security taxes?

Yes. The IRS says Social Security benefits may be taxable when modified adjusted gross income plus one half of benefits is above the base amount for your filing status.

Can withdrawals affect Medicare premiums?

Yes. Higher income from withdrawals, conversions, or capital gains can affect Medicare income-related premium adjustments for some retirees.

Is Roth last always best?

No. Saving Roth for later can be useful, but some retirees may need Roth withdrawals earlier to manage taxes, healthcare costs, or cash flow.

Sources

- IRS, Topic No. 451, Individual Retirement Arrangements: https://www.irs.gov/taxtopics/tc451

- IRS, Required Minimum Distributions FAQs: https://www.irs.gov/retirement-plans/retirement-plan-and-ira-required-minimum-distributions-faqs

- IRS, Topic No. 409, Capital Gains and Losses: https://www.irs.gov/taxtopics/tc409

- IRS, Topic No. 423, Social Security and Equivalent Railroad Retirement Benefits: https://www.irs.gov/taxtopics/tc423