Short Answer

Part-time work can make a retirement plan stronger, but it can also change taxes, healthcare costs, and Social Security benefit timing.

A small amount of earned income may:

- Reduce portfolio withdrawals

- Help bridge the years before Social Security

- Help bridge the years before Medicare

- Give the plan more flexibility in a weak market

- Allow delayed Social Security

- Reduce pressure to sell investments

But earned income can also:

- Affect Social Security benefits if you claim before full retirement age

- Raise taxable income

- Affect ACA Marketplace savings before Medicare

- Affect Medicare IRMAA for some retirees

- Reduce time available for travel, caregiving, or rest

The question is not only whether part-time work adds money. The question is how it changes the whole retirement plan.

Why Part-Time Work Can Help

Part-time work can be powerful because it reduces the amount the portfolio must provide.

For example, earning $20,000 per year from part-time work may reduce withdrawals by $20,000 before tax. That can matter a lot in the first years of retirement, especially if markets are weak.

Part-time work can also help with:

- Healthcare premiums before Medicare

- Delaying Social Security

- Waiting to spend tax-deferred accounts

- Paying taxes on Roth conversions

- Keeping a larger cash reserve

- Reducing anxiety about withdrawals

It can also give some retirees structure and purpose. That part is harder to model, but it still matters.

The Social Security Earnings Test

If you claim Social Security before full retirement age and keep working, the earnings test may matter.

SSA says you can work while receiving Social Security retirement or survivors benefits. But if you are younger than full retirement age and earn more than the yearly earnings limit, SSA may reduce your benefit amount.

For 2026, SSA says:

- If you are under full retirement age for the entire year, the annual earnings limit is $24,480.

- SSA deducts $1 from benefits for every $2 earned above that limit.

- In the year you reach full retirement age, the limit is $65,160 for earnings before the month you reach full retirement age.

- SSA deducts $1 for every $3 earned above that higher limit.

- Starting with the month you reach full retirement age, there is no limit on how much you can earn and still receive benefits.

SSA also says it recalculates your benefit at full retirement age to give credit for months when benefits were reduced or withheld due to excess earnings.

The earnings test does not mean part-time work is bad. It means claiming age and work income should be modeled together.

What Counts For The Earnings Test?

SSA says it counts only wages from your job or net profit if you are self-employed. It includes bonuses, commissions, and vacation pay.

SSA says it does not count pensions, annuities, investment income, interest, veterans benefits, or other government or military retirement benefits for this earnings test.

This distinction matters.

Two retirees could have the same total income, but only one may be affected by the Social Security earnings test if the income comes from wages or self-employment before full retirement age.

Taxes Still Matter

Part-time work can increase taxable income.

It may also change how other income is taxed. The IRS says Social Security benefits may be taxable when modified adjusted gross income plus one half of Social Security benefits is above the base amount for your filing status.

Part-time wages can stack with:

- Social Security

- IRA withdrawals

- 401k withdrawals

- Pension income

- Interest

- Dividends

- Capital gains

- Roth conversions

That does not mean part-time work is a problem. It means the after-tax income matters more than the gross paycheck.

Healthcare Before Medicare

Part-time work can affect early retirees before Medicare.

HealthCare.gov says retirees who lose job-based coverage before age 65 can use the Health Insurance Marketplace to buy a plan. Marketplace savings can depend on income and household size.

That means part-time work may:

- Help pay healthcare premiums

- Raise the income estimate used for Marketplace savings

- Change premium tax credits

- Change eligibility for lower out-of-pocket costs

- Make employer coverage available if the job offers benefits

The healthcare result can go either direction. A job with health benefits can be very valuable. A job without benefits may still help cash flow, but the added income should be tested against Marketplace assumptions.

Medicare And IRMAA

Part-time work after Medicare starts may affect Medicare income-related costs for some retirees.

SSA says people who had a life-changing event that reduced household income can ask to lower their Medicare Part B and Part D income-related monthly adjustment amount. Life-changing events listed by SSA include loss of income and work reduction.

For retirees who keep working part time, the planning point is different:

Income can affect the Medicare cost picture. If part-time income is temporary, the retiree should understand how future income changes may affect IRMAA and whether a life-changing event request later becomes relevant.

The main lesson is simple:

Do not model Medicare costs as fixed if income is changing.

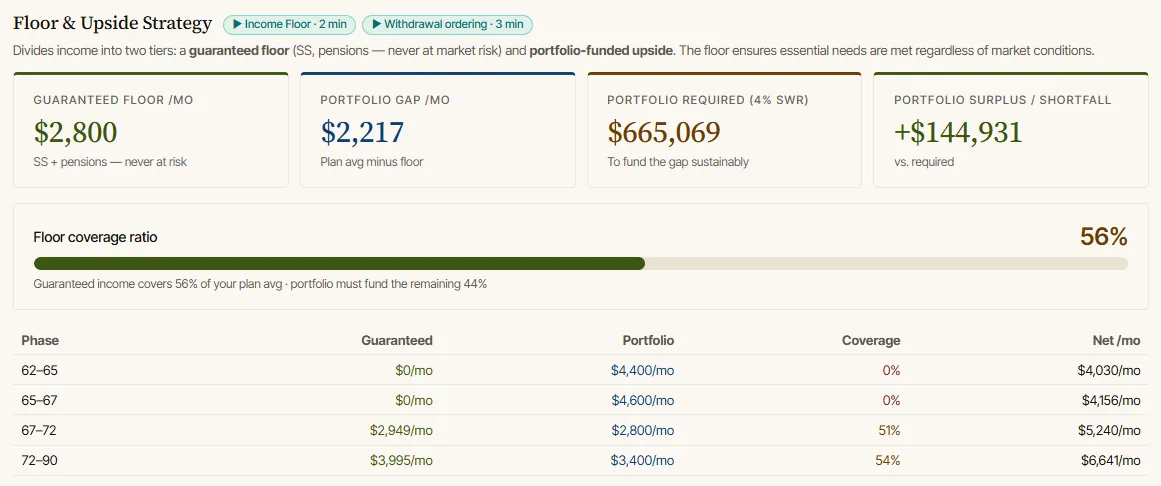

Part-Time Work As A Retirement Bridge

Part-time work can bridge several gaps:

Before Medicare

A part-time job may help cover health insurance before Medicare or provide employer coverage.

Before Social Security

Earned income can reduce withdrawals while waiting to claim Social Security.

Before RMDs

Part-time work can create income during lower-income years, but it may also reduce room for Roth conversions.

During A Market Decline

Working part time during a weak market may reduce withdrawals from a down portfolio.

During A Spouse's Transition

One spouse working part time can help the household retire in stages instead of both stopping work at once.

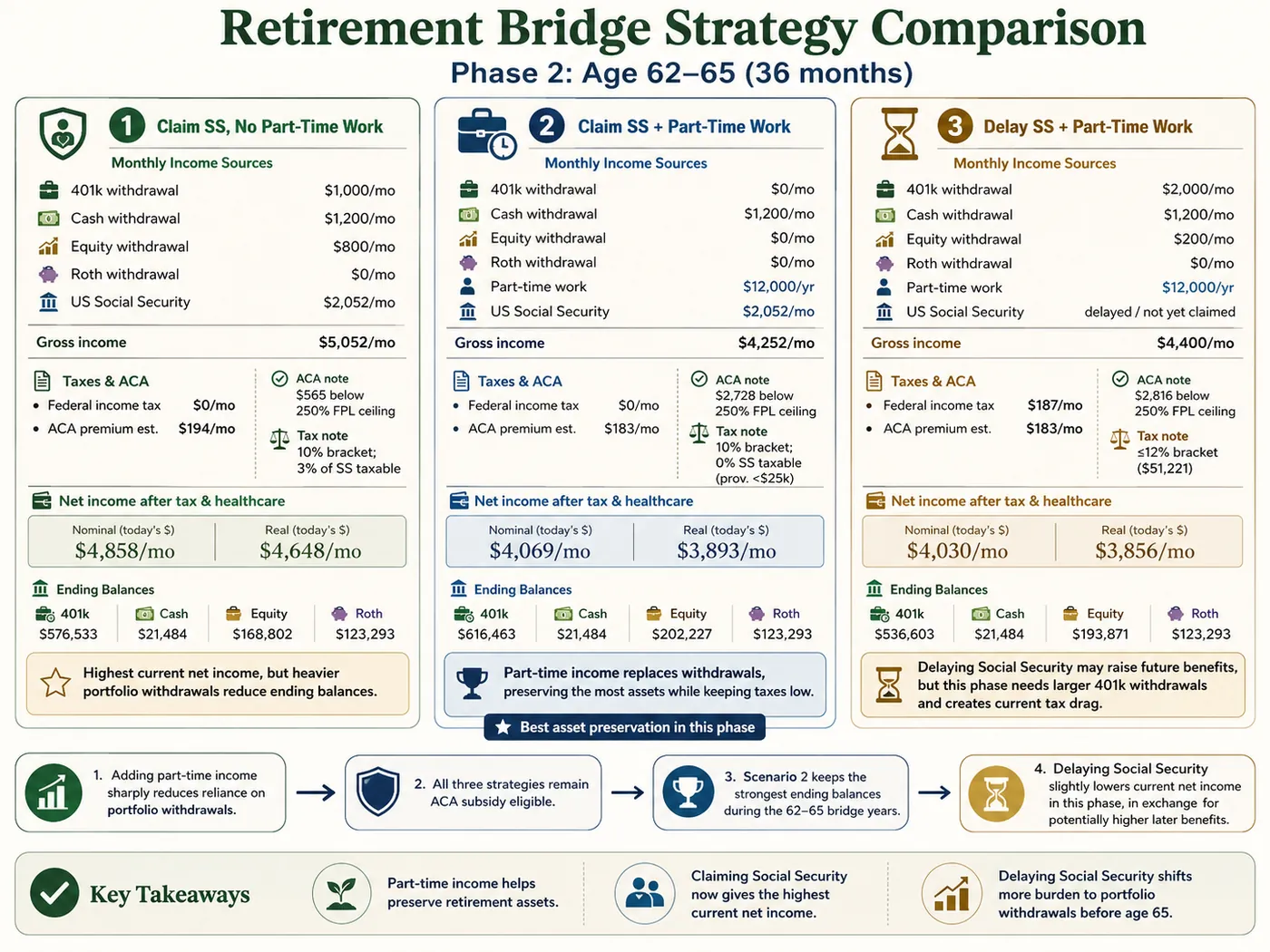

A Simple Example

Suppose a single retiree leaves full-time work at 62.

They can choose:

- Claim Social Security at 62 and take portfolio withdrawals

- Work part time from 62 to 67 and delay Social Security

- Work part time for two years, then claim Social Security at 64

- Take a lower-stress job with health benefits

Each path changes the plan:

- Social Security timing

- Portfolio withdrawals

- Taxable income

- Healthcare costs

- Roth conversion room

- Confidence score

- Stress test results

The best answer depends on the numbers and the retiree's willingness to work.

Part-Time Work And Withdrawal Order

Earned income can change which accounts you withdraw from.

If part-time work covers basic spending, you may withdraw less from:

- Cash

- Taxable brokerage

- Traditional IRA

- 401k

- Roth accounts

That can help preserve assets. But it may also change tax planning.

For example:

- Less IRA withdrawal may mean larger future RMDs.

- More earned income may reduce Roth conversion room.

- Less taxable account selling may reduce capital gains.

- More income may affect ACA or IRMAA planning.

The withdrawal order should be tested with and without part-time income.

Part-Time Work And Stress Testing

Part-time work can be a powerful stress-test lever.

Compare:

- No part-time work

- $10,000 per year for three years

- $25,000 per year until Medicare

- Seasonal work during weak market years

- Consulting income for the first five retirement years

- One spouse working part time while the other retires

Then check:

- Confidence

- Ending balances

- Taxable income

- Healthcare costs

- Social Security timing

- Survivor outcomes

- Plan Health notes

Part-time work does not need to last forever to matter. A few years of income can reduce pressure during the most fragile years.

How To Model Part-Time Work In The Planner

Use this workflow in the AI Retirement Income Planner:

- Build the baseline plan with no part-time work.

- Add planned Social Security claiming ages.

- Add healthcare assumptions before and after Medicare.

- Add part-time earned income for specific years.

- Review Tax & ACA for healthcare and tax effects.

- Use SS Optimizer to compare claiming ages.

- Use the Balance tab to see how part-time income affects your account balances over time.

- Use Scenarios to compare no work, part-time work, and delayed Social Security.

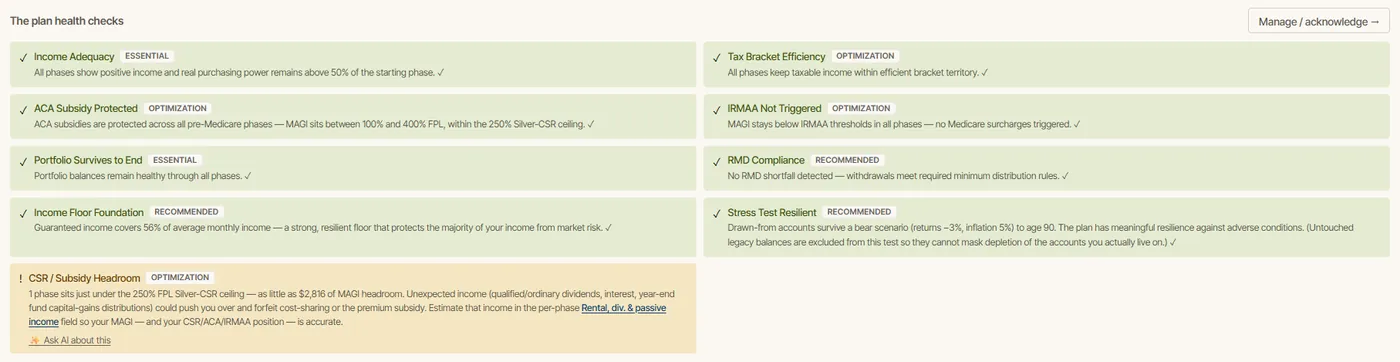

- Use Stress test to see whether part-time work helps in bad markets.

- Open Plan Health and review warnings.

- Check Confidence and ending balances.

- Review survivor outcomes if married.

Part-Time Work Checklist

Before relying on part-time work, answer:

- How many years do I expect to work?

- Is the income realistic?

- Will the work be seasonal, consulting, employee wages, or self-employment?

- Will the job provide health insurance?

- Am I claiming Social Security before full retirement age?

- Will the earnings test apply?

- How will wages affect taxes?

- How will wages affect ACA Marketplace savings?

- Could income affect Medicare IRMAA?

- Does part-time work reduce withdrawals enough to matter?

- Does it reduce Roth conversion room?

- What happens if I cannot keep working?

- What happens if the job disappears?

- Does the plan still work without the income?

FAQ

Can I work while receiving Social Security?

Yes. SSA says you can work while receiving Social Security retirement or survivors benefits. If you are younger than full retirement age and earn more than the annual earnings limit, SSA may reduce your benefit amount.

What is the Social Security earnings limit in 2026?

SSA says the 2026 annual earnings limit is $24,480 if you are under full retirement age for the entire year. In the year you reach full retirement age, the 2026 limit is $65,160 for earnings before the month you reach full retirement age.

Does the earnings test apply after full retirement age?

SSA says starting with the month you reach full retirement age, there is no limit on how much you can earn and still receive benefits.

Does Social Security count investment income for the earnings test?

SSA says it counts wages from work and net profit from self-employment. It does not count pensions, annuities, investment income, interest, veterans benefits, or other government or military retirement benefits for the earnings test.

Can part-time work affect ACA subsidies?

Yes. HealthCare.gov says Marketplace savings are based on income and household size. Part-time income can affect the income estimate used for coverage.

Can part-time work affect Medicare IRMAA?

It can, because IRMAA is income-related. SSA also has a process to request a lower IRMAA amount after certain life-changing events that reduce household income, including work reduction or loss of income.

Is part-time work always good for a retirement plan?

No. It can reduce withdrawals and improve flexibility, but it may affect taxes, healthcare costs, Social Security timing, and lifestyle. Model it before relying on it.

Sources

- SSA, Receiving Benefits While Working: https://www.ssa.gov/benefits/retirement/planner/whileworking.html

- IRS, Topic No. 423, Social Security and Equivalent Railroad Retirement Benefits: https://www.irs.gov/taxtopics/tc423

- HealthCare.gov, Health Coverage For Retirees: https://www.healthcare.gov/retirees/

- SSA, Request To Lower An Income-Related Monthly Adjustment Amount: https://www.ssa.gov/medicare/lower-irmaa