Quick Answer

AI needs a retirement calculator underneath because retirement planning is math, timing, rules, and assumptions before it is conversation.

AI can explain ideas in plain English. It can help you think of scenarios. It can help turn a vague concern into a checklist. It can summarize the result of a plan.

But a retirement plan also needs to calculate:

- Account balances over time.

- Spending by phase.

- Social Security timing.

- Roth conversions.

- Required minimum distributions.

- Federal and state taxes.

- Medicare costs and IRMAA.

- ACA income sensitivity before Medicare.

- Healthcare inflation.

- Survivor income changes.

- Market-risk ranges.

- Historical stress periods.

Those calculations need structured inputs and repeatable math. AI can help you understand the results, but the calculator has to do the measuring.

Key Takeaways

- AI is useful for explanation, organization, and scenario thinking.

- A retirement calculator is needed for repeatable math.

- Retirement planning errors can come from missing one rule, one date, or one account.

- AI text by itself does not prove a retirement plan works.

- OpenAI's ChatGPT FAQ says outputs may be inaccurate or misleading at times.

- Investor.gov warns that AI-generated investment information can be inaccurate, incomplete, misleading, faulty, or made up.

- The best use of AI in retirement planning is as an assistant connected to a structured model, with the user reviewing and approving changes.

Why AI Alone Feels Helpful At First

AI feels useful because retirement planning is confusing.

A person might ask:

- "Can I retire at 62?"

- "Should I delay Social Security?"

- "Would a Roth conversion help?"

- "How much cash should I keep?"

- "What happens if one spouse dies first?"

- "How do Medicare premiums affect my plan?"

AI can answer in a friendly way. It can explain the vocabulary. It can name the moving parts. It can say that taxes, healthcare, inflation, withdrawals, and Social Security all matter.

That is a real benefit.

The problem is that a good explanation is not the same as a calculated plan.

For example, AI can explain why Roth conversions may help before RMDs start. But the useful question is usually more specific:

If I convert $25,000 per year from age 62 through 64, how does that affect my tax bracket, ACA income, Medicare IRMAA exposure later, after-tax balances, and survivor plan?

That is no longer a plain-English question. It is a calculator problem.

What A Retirement Calculator Adds

A real retirement calculator gives AI something concrete to work from.

It turns broad questions into structured inputs:

- Current age.

- Retirement age.

- Life expectancy.

- Account balances.

- Account types.

- Income sources.

- Spending phases.

- Inflation assumptions.

- Tax assumptions.

- Healthcare assumptions.

- Social Security claim ages.

- Pension income.

- Roth conversion amounts.

- One-time expenses or windfalls.

- Survivor assumptions.

Then it applies the same math each time.

That matters because retirement planning is full of tradeoffs where one answer changes another answer.

Delay Social Security and you may need larger portfolio withdrawals early. Convert more to Roth and you may reduce future RMDs, but you may raise near-term taxable income. Retire before Medicare and ACA income may matter more than gross income. Spend more cash early and the stock portfolio may have more time to grow, but cash can run down faster than expected.

AI can talk about those tradeoffs. A calculator can show them.

The Difference Between Text Output And Planner Output

AI text output usually gives you a narrative.

Planner output gives you numbers.

A narrative might say:

- "Delaying Social Security can increase lifetime benefits."

- "Roth conversions may reduce future taxes."

- "Healthcare costs can be a major retirement risk."

- "Sequence risk matters early in retirement."

Planner output can show:

- Ending balances by year.

- Cash, taxable, Roth, and 401(k) balances.

- Annual withdrawal amounts.

- Estimated taxes.

- Medicare and IRMAA impact.

- ACA sensitivity before Medicare.

- RMD estimates.

- Probability ranges from Monte Carlo.

- Historical backtest outcomes.

- Plan Health warnings.

- Scenario comparisons.

Both are useful, but they are not interchangeable.

In a high-stakes topic, words without numbers can sound more certain than they are.

Example 1: Retiring Before Medicare

Say someone wants to retire at 62.

AI can explain the bridge years between 62 and 65:

- There may be no employer coverage.

- ACA marketplace coverage may matter.

- Taxable income can affect subsidies.

- Roth conversions can affect income.

- Cash withdrawals may be useful in some years.

But the planner has to calculate the years.

The key question is not "Is retiring at 62 possible?" The better question is:

What happens to cash, taxes, healthcare cost, ACA income, and later portfolio balance if retirement starts at 62 instead of 65?

That needs a model that can compare taxes and healthcare across both scenarios, not a single paragraph of advice.

Example 2: Roth Conversions

Roth conversions are a good example of why AI needs calculator support.

AI can explain that converting pre-tax money to Roth may help in lower-income years. It can also explain that conversion income may affect tax brackets, ACA subsidies, Medicare IRMAA, and cash flow.

But deciding whether a conversion is worth testing depends on numbers:

- How much pre-tax money exists?

- What is the current tax bracket?

- When do RMDs start?

- Is there a pre-Medicare ACA period?

- Is Medicare IRMAA close?

- What is the survivor tax situation?

- What assets pay the conversion tax?

- How does the plan look if markets are poor early?

A calculator can test a conversion amount inside the whole plan. AI can then help explain why the result improved, got worse, or stayed roughly the same.

Example 3: Social Security Timing

AI can explain the basic Social Security tradeoff:

- Claim earlier and income starts sooner.

- Claim later and monthly benefits may be higher.

- Couples need to think about survivor income.

- Break-even age is only one part of the decision.

But the calculation depends on the household.

For a couple, the best-looking choice for the first spouse may be weaker when survivor income is included. A higher earner's delayed benefit may protect the surviving spouse. A lower earner's claim age may matter differently.

A calculator can compare claim ages and show the effect on portfolio withdrawals, taxes, survivor income, and ending balances. AI can help interpret the result in plain English.

Why Calculator-Backed AI Is Safer

Calculator-backed AI is safer because the AI has boundaries.

Instead of asking an AI tool to invent a retirement plan from a paragraph, the workflow becomes:

- Enter the household facts into the planner.

- Run the calculator.

- Review the plan output.

- Ask AI to explain a specific result.

- Test a specific change.

- Compare before and after.

- Apply the change only after review.

That keeps the AI in the role where it is most useful: explaining, organizing, and proposing things to test.

It also keeps the calculator in the role where it is strongest: applying the same math to the same facts each time.

Where AI Still Needs Caution

Even when AI is useful, it needs caution.

General chatbots are the clearest example. A tool like ChatGPT can help with retirement planning as an explainer, and our guide on whether ChatGPT can help with retirement planning shows where it helps and where it should not, but OpenAI's ChatGPT FAQ says model outputs may be inaccurate, untruthful, or otherwise misleading at times, and that ChatGPT can occasionally produce incorrect answers. The same page also says users should avoid sharing sensitive information in conversations.

OpenAI's Data Controls FAQ explains that users can control whether their ChatGPT conversations help improve models, and that Temporary Chats have different retention and training behavior than regular chats.

Investor.gov warns that AI-generated investment information can be inaccurate, incomplete, misleading, faulty, or made up.

Those cautions matter in retirement planning because the output can sound polished even when a rule, date, or assumption is wrong.

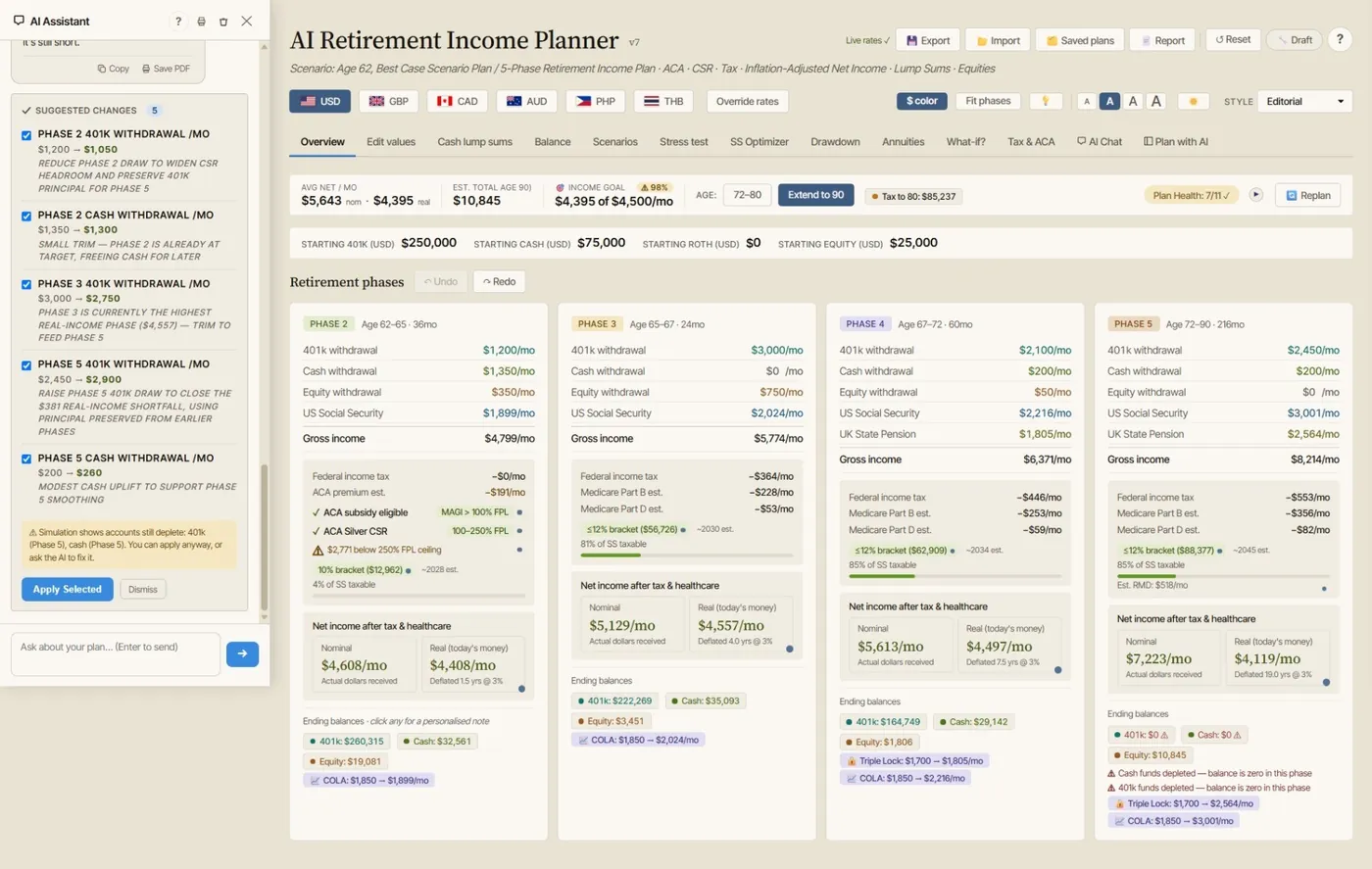

How The AI Retirement Income Planner Handles This

The AI Retirement Income Planner is built around the idea that AI should sit beside the calculator.

The planner first models the retirement plan using structured inputs and a month-by-month engine. It includes planning areas such as:

- Five retirement phases.

- Income and withdrawals.

- Account balances.

- Taxes.

- ACA and healthcare costs.

- Medicare and IRMAA.

- Social Security.

- Spouse Social Security.

- Roth conversions.

- RMD estimates.

- State tax assumptions.

- Lump sums and major expenses.

- Scenarios.

- Stress tests.

- Monte Carlo.

- Historical backtesting.

- Plan Health.

- Plan Confidence.

Then the optional AI features can help explain or propose changes.

The AI Chat tab can be used for plan questions, plan review, Learn-the-planner mode, and proposal workflows. The Plan with AI sidebar can work beside planner tabs. The planner can propose numeric changes, but the user reviews and approves changes.

That structure is important. The AI is not floating above the plan. It is connected to the plan.

A Practical Way To Use AI With Retirement Math

Here is a better workflow than asking AI, "Can I retire?"

Start with a specific calculator-backed question:

- "Compare retiring at 62 versus 65."

- "Test claiming Social Security at 67 versus 70."

- "Test a smaller Roth conversion before Medicare."

- "Show the survivor version of this plan."

- "Compare higher healthcare inflation."

- "Run a stress test with weaker early returns."

Then use AI for the follow-up:

- "Explain why the 62 scenario runs cash down faster."

- "Summarize the biggest Plan Health warning."

- "List three assumptions I should verify."

- "Turn this result into questions for my tax professional."

- "Explain why Medicare IRMAA changed in this scenario."

- "Summarize the difference between these two plans."

That workflow gets the best of both tools.

The calculator keeps the numbers grounded. AI helps the human understand the meaning.

What To Look For In An AI Retirement Calculator

If you are comparing AI retirement planning tools, this checklist for what an AI retirement planner should and should not do covers the full picture, but look for these traits:

- Structured inputs instead of a chat box alone.

- Year-by-year or month-by-month calculations.

- Separate account types.

- Social Security timing tools.

- Roth conversion testing.

- RMD handling.

- Tax modeling.

- Healthcare and Medicare assumptions.

- ACA sensitivity if retiring before Medicare.

- Scenario comparison.

- Stress testing.

- Monte Carlo or historical risk tools.

- Clear assumptions.

- Export or report features.

- User review before AI-proposed changes are applied.

- Plain-language explanations beside the numbers.

The key question is simple:

Can the tool show how it got the result?

If the answer is no, treat the output as a conversation starter, not a plan.

FAQ

Can AI replace a retirement calculator?

No. AI can help explain retirement planning, but a retirement calculator is needed to run structured math across taxes, healthcare, Social Security, withdrawals, balances, and risk.

Is ChatGPT a retirement calculator?

ChatGPT can discuss retirement planning concepts, but it is not the same as a dedicated retirement calculator. OpenAI's ChatGPT FAQ warns that outputs may be inaccurate or misleading at times.

What is an AI retirement calculator?

An AI retirement calculator is best understood as a calculator-backed planning tool with AI assistance. The calculator runs the numbers. AI helps explain results, organize questions, and test user-reviewed scenarios.

Why does Social Security need calculator support?

Social Security timing affects income, portfolio withdrawals, taxes, survivor planning, and longevity risk. Couples may need to compare many primary and spouse claim-age combinations.

Why do Roth conversions need calculator support?

Roth conversions affect taxable income, future RMDs, ACA income, Medicare IRMAA, account balances, survivor taxes, and cash flow. The right amount to test depends on the full plan.

What should I ask AI after running a retirement calculator?

Ask AI to explain a specific result, identify assumptions to verify, summarize differences between scenarios, or prepare questions for a qualified professional.

Source Links

- OpenAI, ChatGPT General FAQ: https://help.openai.com/en/articles/6783457-chatgpt-general-faq

- OpenAI, Data Controls FAQ: https://help.openai.com/en/articles/7730893-data-controls-faq

- NIST, AI Risk Management Framework: https://www.nist.gov/itl/ai-risk-management-framework

- Investor.gov, Artificial Intelligence and Investment Fraud: https://www.investor.gov/introduction-investing/general-resources/news-alerts/alerts-bulletins/investor-alerts/artificial-intelligence-fraud

- AI Retirement Income Planner official site: https://airetirementincomeplanner.com/

- AI-Ready Retirement Income Planner product overview: https://webnomad.webflow.io/pages/ai-ready-retirement-income-planner

Bottom Disclaimer

This article is for general education only. It is not financial, tax, investment, legal, healthcare, insurance, privacy, cybersecurity, Social Security, estate, AI safety, or retirement advice. Verify important decisions with official sources, qualified professionals, and your own planning assumptions.