Quick Answer

Retirement withdrawal guardrails are pre-set rules for adjusting spending or withdrawals when the plan gets stronger or weaker.

A simple guardrail plan might say:

- If portfolio balances fall below a warning level, reduce travel spending by 20 percent for one year

- If inflation runs higher than expected, delay a large purchase

- If healthcare costs rise, pause optional gifts or home upgrades

- If the plan becomes much stronger, increase discretionary spending within a set limit

- If taxes spike, change the withdrawal mix before taking extra IRA withdrawals

Guardrails help retirees avoid making rushed decisions during market downturns, healthcare surprises, inflation shocks, or tax-heavy years.

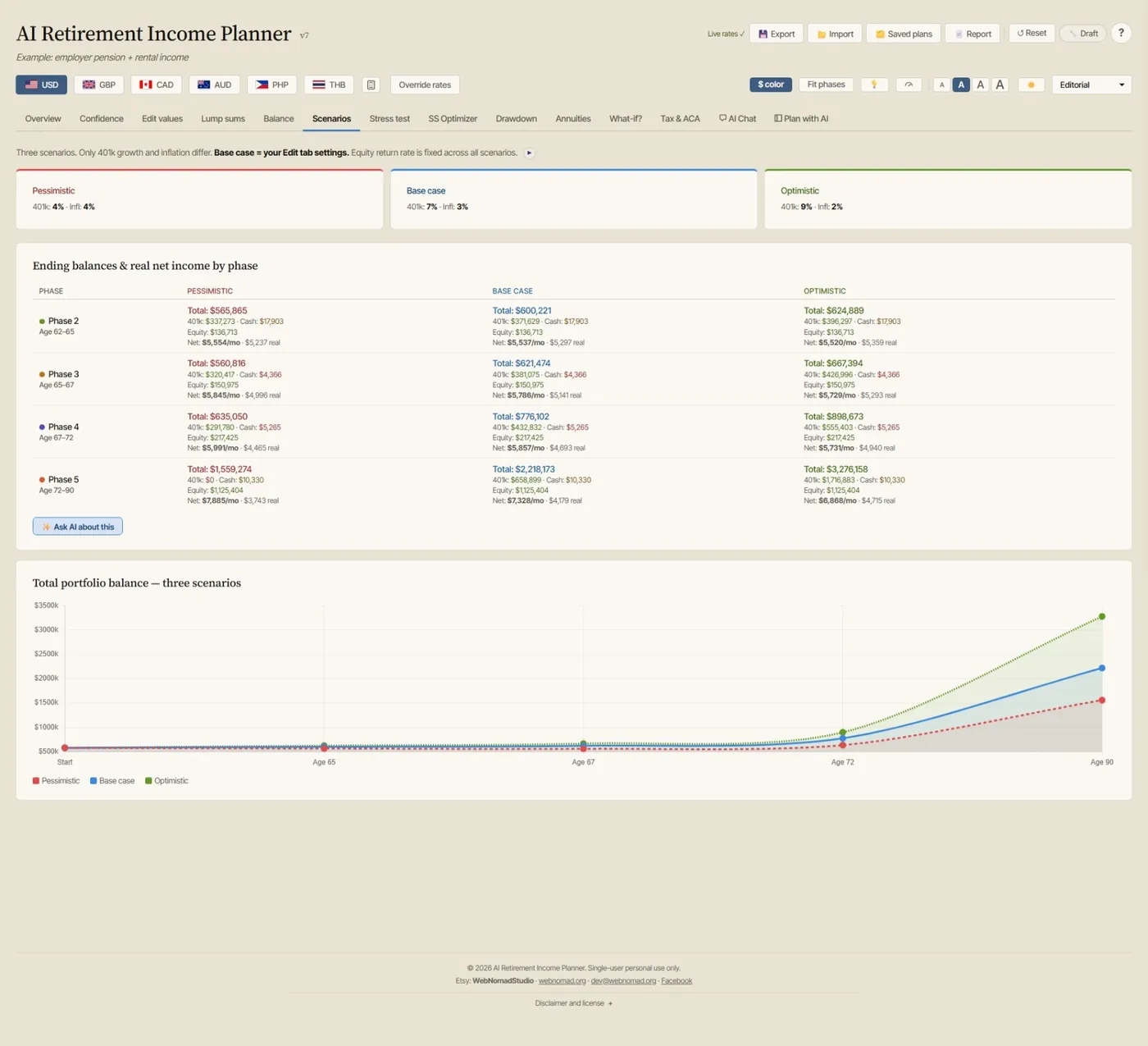

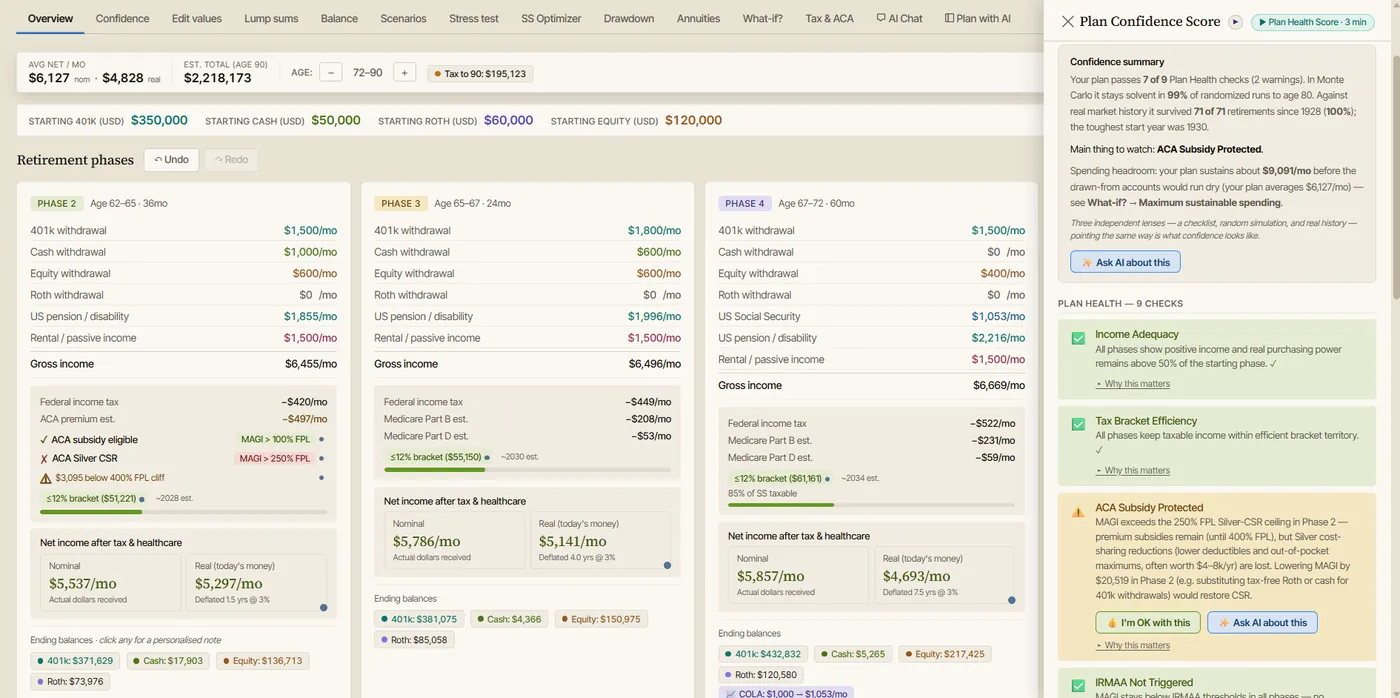

The AI Retirement Income Planner helps by letting you create base and fallback scenarios, test market and inflation stress, review drawdown order, check taxes, compare confidence scores, and use Plan Health to identify weak spots.

Why Guardrails Matter In Retirement

Retirement is not a one-time calculation.

Even a careful plan can be affected by:

- Market declines

- Higher inflation

- Healthcare surprises

- Long life

- Lower investment returns

- Social Security claiming choices

- RMDs

- Tax law changes

- Home repairs

- Family support

- One spouse dying earlier than expected

Investor.gov explains that investing involves uncertainty and potential financial loss. It also describes risks such as volatility risk, inflation risk, liquidity risk, and interest rate risk. Those risks matter more in retirement because money is leaving the plan while conditions keep changing.

Guardrails turn uncertainty into a response plan.

Instead of asking, "What should I do now?" during a bad year, the retiree can follow rules that were chosen calmly.

What A Withdrawal Guardrail Is

A withdrawal guardrail is a rule that tells you when to adjust the plan.

It usually has three parts:

- A trigger

- An action

- A review date

Example:

- Trigger: Portfolio balance falls 15 percent below the planned year-end balance

- Action: Reduce discretionary spending by $8,000 for the next 12 months

- Review date: Recheck the plan at the next annual review or after balances recover

The guardrail does not need to be complicated. It needs to be clear enough to use.

Good guardrails are specific. Weak guardrails are vague.

"Spend less if things look bad" is vague.

"If the plan confidence score drops below the target range, pause the next vehicle upgrade and reduce travel by $500 per month for one year" is useful.

Guardrails Are Not The Same As A Fixed Withdrawal Rate

A fixed withdrawal rate says you withdraw a set amount or percentage, often adjusted for inflation.

A guardrail strategy says the withdrawal can change when the plan changes.

That flexibility is useful because how much you can spend in retirement is not always fixed. Some expenses must be paid, but others can move.

Essential expenses:

- Housing

- Food

- Utilities

- Insurance

- Healthcare

- Taxes

- Transportation

Flexible expenses:

- Travel

- Dining out

- Hobbies

- Gifts

- Home upgrades

- New vehicles

- Large optional purchases

Guardrails protect essential expenses first, then adjust flexible expenses when needed.

Step 1: Separate Essential And Flexible Spending

Guardrails are hard to use if all spending is one number.

Start by separating:

- Must-pay spending

- Should-pay spending

- Nice-to-have spending

Must-pay spending includes basic living costs, healthcare, taxes, insurance, and debt payments.

Should-pay spending includes maintenance, vehicle replacement, dental care, home repairs, and family support that is hard to avoid.

Nice-to-have spending includes travel, hobbies, gifts, upgrades, and other discretionary items.

The planner can help by modeling recurring expenses, healthcare, taxes, and lump sum events separately. That makes it easier to decide what changes first if the plan weakens.

Step 2: Choose The Triggers

A trigger is the condition that starts a review.

Possible guardrail triggers include:

- Portfolio balance is below the planned range

- Confidence score falls below a chosen level

- Annual withdrawal rate rises above a chosen level

- Cash reserve falls below 6 or 12 months of spending

- Healthcare costs rise above the planned amount

- Inflation is higher than expected

- A large expense arrives early

- One spouse dies

- RMDs create a tax spike

- Medicare IRMAA exposure appears

- ACA premium tax credits are at risk before Medicare

Triggers should be measurable. If the trigger is too subjective, it may be ignored.

The AI Retirement Income Planner can help by showing account balances, drawdown, stress tests, confidence, taxes, and plan health warnings.

Step 3: Choose The Actions

Once a trigger is met, the plan needs a specific action.

Possible actions include:

- Reduce travel spending for one year

- Delay a vehicle purchase

- Pause major home upgrades

- Reduce gifts temporarily

- Use cash reserves

- Change withdrawal sources

- Reduce Roth conversion amount

- Claim Social Security earlier than planned

- Work part time

- Delay retirement

- Downsize earlier

- Buy or avoid an income product

- Rebalance the portfolio

- Meet with a tax or financial professional

The action should match the trigger.

If a market decline is the issue, reducing discretionary spending and using cash may help. If taxes are the issue, changing withdrawal sources may help. If healthcare costs are the issue, the plan may need a healthcare-specific adjustment.

Step 4: Choose The Review Schedule

Guardrails need review dates.

Common review points:

- Once per year

- After a market decline

- Before Social Security claiming

- Before Medicare enrollment

- Before RMD years

- After a spouse dies

- Before a large purchase

- After a major tax law change

- After a health change

Without a review schedule, guardrails can become stale.

The planner's Report button can help document assumptions and decisions so the next review starts from a clear record.

Market Guardrails

Market guardrails help manage bad investment years.

Possible triggers:

- Portfolio falls more than 10 percent from the plan projection

- First retirement year has negative returns

- Cash reserve falls below the target

- Withdrawal rate rises above a chosen level

Possible actions:

- Use cash reserve for a set period

- Reduce travel spending

- Delay a large purchase

- Avoid selling heavily declined assets if possible

- Rebalance if the investment plan calls for it

- Review Social Security timing

Investor.gov's risk guidance is a useful reminder that investments can fluctuate and that liquidity matters. A market guardrail should reduce forced selling when possible, while still paying the bills.

Inflation Guardrails

Inflation guardrails help when costs rise faster than expected.

Possible triggers:

- Annual spending rises more than planned

- Healthcare costs exceed the planned inflation assumption

- Essential spending rises faster than reliable income

- Portfolio withdrawals increase faster than expected

Possible actions:

- Reduce flexible spending

- Delay optional purchases

- Review insurance, utilities, and subscriptions

- Revisit the cash reserve

- Adjust future inflation assumptions

- Update the retirement income floor

Inflation guardrails are useful because they stop a spending plan from drifting upward year after year with no review.

Healthcare Guardrails

Healthcare needs its own guardrails.

Medicare.gov explains that Medicare costs can include premiums, deductibles, coinsurance, copayments, and prescription drug costs. Before Medicare, retirees may have Marketplace coverage, COBRA, retiree coverage, spouse employer coverage, or private insurance.

Possible healthcare triggers:

- Premiums rise above the planned amount

- Out-of-pocket costs exceed the reserve

- A new prescription changes annual spending

- Income threatens ACA premium tax credits

- Income triggers or increases Medicare IRMAA

- Long-term care costs become likely

Possible actions:

- Re-shop coverage during enrollment windows

- Adjust taxable withdrawals

- Pause Roth conversions

- Use cash instead of taxable withdrawals

- Reduce discretionary spending

- Add a healthcare-specific reserve

- Ask for professional tax or insurance advice

Healthcare guardrails matter because these costs are often less flexible than travel or hobbies.

Tax Guardrails

Tax guardrails help prevent withdrawals from creating avoidable problems.

Possible triggers:

- Taxable income jumps above the plan

- A Roth conversion pushes income too high

- Capital gains are larger than expected

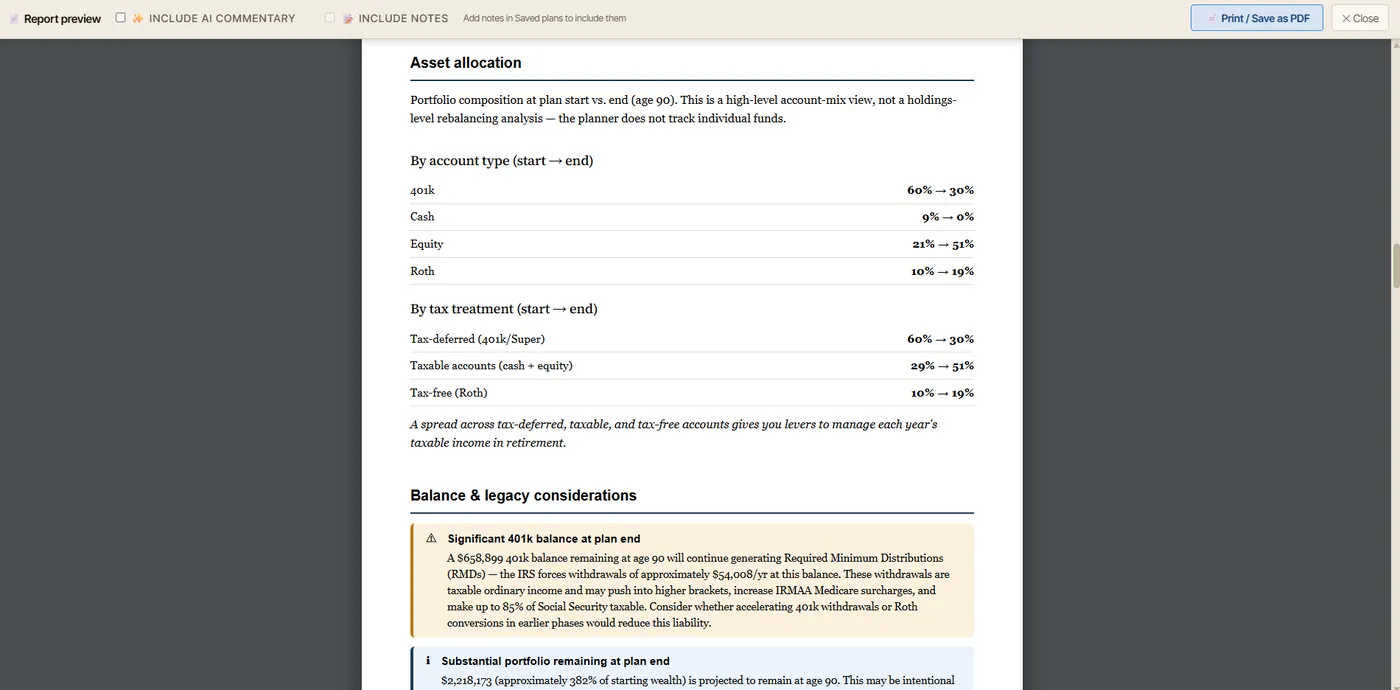

- RMDs begin

- Social Security taxation increases

- Medicare IRMAA appears

- ACA subsidies are reduced

The IRS explains that retirement account owners generally must take required minimum distributions once RMD rules apply. RMDs can affect taxable income, so later-life guardrails should include them.

Possible actions:

- Reduce Roth conversion amount

- Change withdrawal order

- Use taxable cash before IRA withdrawals

- Harvest gains or losses when appropriate

- Spread income across multiple years

- Delay a large sale

- Get tax advice before year-end

The planner's Tax & ACA tab can help identify years where taxable income rises.

Social Security Guardrails

Social Security timing can be part of a guardrail plan.

The Social Security Administration says retirement benefits can start as early as age 62, but benefits started before full retirement age are reduced. Delaying beyond full retirement age can increase benefits up to age 70.

Possible triggers:

- Portfolio withdrawals are higher than expected before Social Security starts

- Market losses make a delayed claiming plan weaker

- Cash reserves fall below the target

- A spouse's survivor income needs more protection

- Health or work plans change

Possible actions:

- Claim earlier than originally planned

- Delay if the plan remains strong

- Claim one spouse's benefit earlier and delay the other, if appropriate

- Use cash reserves to preserve a delayed claiming plan

- Reduce spending during the bridge years

Social Security guardrails should be tested carefully because claiming decisions can affect lifetime income and survivor income.

Cash Reserve Guardrails

Cash reserve guardrails help decide when cash is doing its job and when it needs rebuilding.

Possible triggers:

- Cash falls below 6 months of essential spending

- Cash falls below 12 months of planned withdrawals

- A large expense uses more cash than planned

- Markets recover after cash was used

Possible actions:

- Refill cash from taxable investments

- Reduce discretionary spending until cash is rebuilt

- Pause large purchases

- Use RMDs to refill cash

- Use part-time income to rebuild cash

Cash can reduce forced selling during bad markets, but cash also has inflation risk. A guardrail plan should say both when to use cash and when to rebuild it.

Spending Increase Guardrails

Guardrails are not only about cutting spending.

If the plan becomes much stronger, a retiree may want to spend more intentionally.

Possible triggers:

- Confidence score rises above the target range

- Portfolio balance exceeds the plan by a set percentage

- Essential expenses are covered by reliable income

- Stress tests remain strong

- Survivor plan remains healthy

Possible actions:

- Increase travel spending within a limit

- Make gifts within a planned range

- Upgrade housing or vehicle plans

- Increase charitable giving

- Fund family goals

- Reduce investment risk

This is important because some retirees underspend out of fear. A good guardrail system can give permission to spend when the plan supports it.

Example: A Guardrail Plan For A Couple

Assume a couple retires at 63 and 61.

They have:

- $95,000 desired annual spending before taxes

- $100,000 in cash

- $400,000 in taxable investments

- $900,000 in traditional retirement accounts

- $250,000 in Roth accounts

- Social Security planned at full retirement age

- One spouse needs health insurance before Medicare

- Travel spending of $16,000 per year for the first five years

Their guardrail plan might include:

- If portfolio balances fall 15 percent below plan, reduce travel by $8,000 for one year

- If cash falls below $50,000, pause major gifts and home upgrades

- If ACA income thresholds are at risk, reduce Roth conversion amount

- If healthcare costs exceed plan by $5,000, delay the vehicle purchase

- If confidence rises above the target range for two reviews, increase travel by $4,000 per year

The couple can model each action in the planner as a scenario.

Example: A Guardrail Plan For A Single Retiree

Assume a single retiree is age 67.

She has:

- $68,000 of annual spending before taxes

- Social Security already started

- Medicare in place

- $75,000 in cash

- $550,000 in traditional retirement accounts

- $250,000 in taxable investments

- $100,000 in Roth accounts

- A paid-off home

Her guardrails might focus less on bridge years and more on healthcare, taxes, home repairs, and long life.

Possible guardrails:

- Keep at least $45,000 in cash

- If home repairs exceed $15,000, reduce travel for one year

- If taxable income approaches an IRMAA threshold, review withdrawals before year-end

- If portfolio balance falls below a chosen level, pause inflation increases on discretionary spending

- If RMDs exceed spending needs, move excess to cash reserve or taxable savings

The right guardrails depend on the retiree's goals and comfort level.

How The AI Retirement Income Planner Helps

The AI Retirement Income Planner can help turn guardrails into visible retirement scenarios.

A practical workflow:

- Build the base retirement plan.

- Separate essential and discretionary spending.

- Enter Social Security, pensions, annuities, rental income, or part-time work.

- Add cash, taxable, traditional retirement, and Roth balances.

- Add healthcare, tax, and inflation assumptions.

- Review Balance and Drawdown.

- Run Stress test scenarios.

- Check Confidence and Plan Health.

- Create a lower-spending fallback scenario.

- Create a higher-spending good-outcome scenario.

- Create tax and healthcare guardrail scenarios.

- Compare reports.

- Write down trigger points and actions.

This makes the guardrail plan practical instead of theoretical.

A Simple Guardrail Worksheet

Use this worksheet:

- Essential annual spending:

- Flexible annual spending:

- Current portfolio balance:

- Planned withdrawal amount:

- Cash reserve target:

- Minimum cash reserve:

- Confidence score target:

- Portfolio warning level:

- Healthcare cost warning level:

- Taxable income warning level:

- Spending cut if warning is triggered:

- Spending increase if plan is stronger:

- Review month each year:

- Professional to call if tax or insurance issue appears:

- Notes for surviving spouse:

Keep the worksheet short enough to use.

Common Mistakes

Common guardrail mistakes include:

- Using vague triggers

- Cutting essential spending before discretionary spending

- Forgetting healthcare costs

- Ignoring taxes

- Ignoring RMD years

- Treating Social Security claiming as separate from withdrawals

- Holding too little cash for bad market years

- Holding too much cash without testing inflation

- Never allowing spending increases when the plan improves

- Failing to write the rules down

- Changing the rules during a panic

Guardrails work best when they are chosen before emotions are high.

FAQ

What are retirement withdrawal guardrails?

Retirement withdrawal guardrails are pre-set rules for adjusting spending, withdrawals, or account use when the retirement plan becomes stronger or weaker.

Are withdrawal guardrails better than the 4 percent rule?

They answer a different problem. A fixed withdrawal rule gives a starting withdrawal method. Guardrails help adjust the plan when markets, inflation, healthcare, taxes, or account balances change.

What is an example of a withdrawal guardrail?

One example is reducing discretionary spending by a set amount if portfolio balances fall below a warning level. Another is delaying a large purchase if healthcare costs rise above the plan.

Should guardrails include Social Security?

Yes, sometimes. Social Security timing can affect portfolio withdrawals, income security, and survivor benefits. It should be tested with the rest of the plan.

Should guardrails include taxes?

Yes. Withdrawals from traditional retirement accounts, Roth conversions, capital gains, RMDs, Social Security taxation, ACA subsidies, and Medicare IRMAA can all affect spendable income.

Can guardrails allow spending increases?

Yes. A good guardrail plan can include rules for increasing discretionary spending when the plan is stronger than expected and stress tests still look healthy.

How often should I review withdrawal guardrails?

Review them at least once per year and after major changes such as a market decline, health event, tax law change, spouse's death, Social Security claiming decision, or large purchase.

How do I model guardrails in a retirement planner?

Create a base scenario, then create fallback and upside scenarios. Change spending, withdrawals, Social Security timing, cash use, healthcare assumptions, and taxes to see how each guardrail affects the plan.

Suggested Product CTA

Want a retirement plan that adapts instead of breaking under stress? The AI Retirement Income Planner lets you build base, fallback, and upside scenarios, test withdrawals, taxes, healthcare, Social Security timing, inflation, and plan health privately in your browser.

Sources And References

- Investor.gov, "What is Risk?": https://www.investor.gov/introduction-investing/investing-basics/what-risk

- Internal Revenue Service, "Retirement plan and IRA required minimum distributions FAQs": https://www.irs.gov/retirement-plans/retirement-plan-and-ira-required-minimum-distributions-faqs

- Social Security Administration, "Starting Your Retirement Benefits Early": https://www.ssa.gov/benefits/retirement/planner/agereduction.html

- Medicare.gov, "Costs": https://www.medicare.gov/basics/costs/medicare-costs