Short Answer

The best way to compare retiring in the US versus abroad is to build both plans side by side. Use the same ages, account balances, Social Security assumptions, pensions, spending goals, and risk settings. Then change the variables that actually differ: taxes, healthcare, housing, currency, insurance, travel, bank accounts, inflation, and whether you might return to the United States later.

The cheaper-looking plan is not always the stronger plan. The stronger plan is the one that still works after healthcare, taxes, exchange rates, and relocation risks are modeled.

Key Takeaways

- Start with a US baseline before building the abroad scenario.

- Compare after-tax income, not headline cost of living.

- Medicare coverage outside the United States is limited.

- Currency risk can change the real cost of living abroad.

- Social Security abroad should be checked with SSA rules and tools.

- A return-to-US scenario should be included even if the move feels permanent.

- The planner can compare saved scenarios with Stress Test, Plan Health, and Plan Confidence.

Why A Simple Cost-Of-Living Comparison Is Weak

Many retiring-abroad comparisons start with rent, groceries, restaurants, and transportation. Those numbers matter, but they are only part of the decision.

A complete comparison should include:

- Taxes on retirement income.

- Healthcare premiums and out-of-pocket care.

- Medicare limits outside the United States.

- Social Security payment rules abroad.

- Exchange-rate changes.

- Housing deposits, leases, sale costs, and relocation costs.

- Travel back to see family.

- Emergency travel.

- Local banking and account reporting.

- Estate documents and beneficiary planning.

- Long-term care.

- The cost of moving back.

A lower rent bill can be overwhelmed by higher healthcare costs, a weaker dollar, lost access to a familiar care network, or a costly return-home move.

Step 1: Build The US Baseline

Start with the plan you already understand: retiring in the United States.

Model:

- Current or expected retirement state.

- Federal tax.

- State tax, if relevant.

- Social Security timing.

- Pension income.

- IRA and 401k withdrawals.

- Roth withdrawals.

- Taxable brokerage income.

- Medicare costs after 65.

- Pre-Medicare healthcare, if retiring early.

- Housing.

- Transportation.

- Travel.

- Long-term care assumptions.

This baseline is the control case. The abroad plan should beat or improve on this plan after taxes, healthcare, risk, and lifestyle tradeoffs are included.

Step 2: Build The Abroad Scenario

Next, duplicate the US baseline and change only the assumptions that would differ abroad.

Change:

- Planning currency.

- Housing cost.

- Local spending.

- Foreign-residence healthcare assumptions.

- Private insurance.

- Medical evacuation.

- Currency exchange rate.

- Local tax assumptions.

- Travel back to the United States.

- Foreign bank account assumptions.

- Return-home cost.

Keep the same starting balances, ages, and Social Security decisions at first. This makes the difference between scenarios easier to understand.

Step 3: Compare Taxes

Taxes can change the answer quickly.

For many US retirees, the starting point is that US citizens and resident aliens abroad are generally subject to US tax on worldwide income. That means the abroad scenario should not simply erase US tax.

Compare:

- US federal tax.

- State tax exposure.

- Foreign tax on pension income.

- Foreign tax on IRA or 401k withdrawals.

- Foreign tax on Social Security.

- Foreign Tax Credit assumptions.

- Tax treaty questions.

- Reporting tasks for foreign accounts.

- Currency conversion for tax reporting.

Some foreign tax systems may be favorable to retirees. Others may tax income differently than expected. Do not assume the local cost-of-living article has answered the tax question, and use a retirement calculator that models taxes and healthcare together rather than a single spending estimate.

Step 4: Compare Healthcare

Healthcare is often the swing factor.

Medicare.gov says Medicare usually does not cover healthcare while traveling outside the United States, with limited exceptions. CDC travel guidance separates travel health insurance, travel disruption coverage, and medical evacuation insurance.

Compare:

- Medicare-based healthcare in the United States.

- Local routine care abroad.

- Private international insurance.

- Prescription costs.

- Emergency hospital costs.

- Medical evacuation coverage.

- Travel back to the United States for care.

- Long-term care.

- Return-to-US healthcare later in life.

This is where a cheap-abroad plan can become more complex. Routine care may be affordable, but major care and insurance structure still need a real model, the same way health insurance before Medicare needs its own plan for an early US retirement.

Step 5: Compare Currency Risk

If retirement income is in dollars and spending is in another currency, exchange rates become part of the retirement plan.

Build at least three abroad versions:

- Base exchange rate.

- Weaker-dollar case.

- Stronger-dollar case.

Then add a fourth version that combines weaker dollar plus higher healthcare costs. That combined scenario is often more useful than a currency-only test.

The question is not whether one exchange rate is right. The question is whether the plan remains workable across a reasonable range of currency outcomes, which is the same idea behind Monte Carlo and historical backtesting: test the plan against many outcomes, not one.

Step 6: Compare Social Security Abroad

Social Security can be payable outside the United States in many situations, but the result depends on the person's facts and destination. SSA provides a Payments Abroad Screening Tool to help people check whether payments may continue outside the United States.

Model Social Security as:

- A USD income stream.

- A benefit that may be spent in a different currency.

- A survivor-income factor for couples.

- A taxable income source.

- A payment stream that should be checked against SSA rules before moving.

For couples, also compare what happens after the first spouse dies. The survivor version of the abroad plan may look different from the couple version, and the underlying question of when to claim Social Security still applies wherever you live.

Step 7: Compare Housing And Family Travel

Housing abroad may be cheaper, but the full comparison should include transition costs.

Compare:

- Selling a US home.

- Renting out a US home.

- Keeping a US home vacant.

- Buying abroad.

- Renting abroad.

- Local deposits and furnishings.

- Storage.

- Moving costs.

- Family travel.

- Emergency travel.

- Visitor costs if family comes to you.

Family travel is easy to understate. If the plan depends on frequent long-haul travel, it should be in the annual budget.

Step 8: Compare The Return-To-US Case

Even a confident move abroad should include a return-home case.

A return may happen because of:

- Healthcare.

- Long-term care.

- Widowhood.

- Family needs.

- Visa or residency changes.

- Safety concerns.

- Exchange-rate pressure.

- Loneliness or lifestyle mismatch.

Model return costs:

- Flights.

- Shipping or storage.

- US housing setup.

- Healthcare transition.

- Vehicle purchase or lease.

- State tax assumption.

- Temporary double housing.

- Professional help.

If the abroad plan works only when the move is permanent, the risk may be understated.

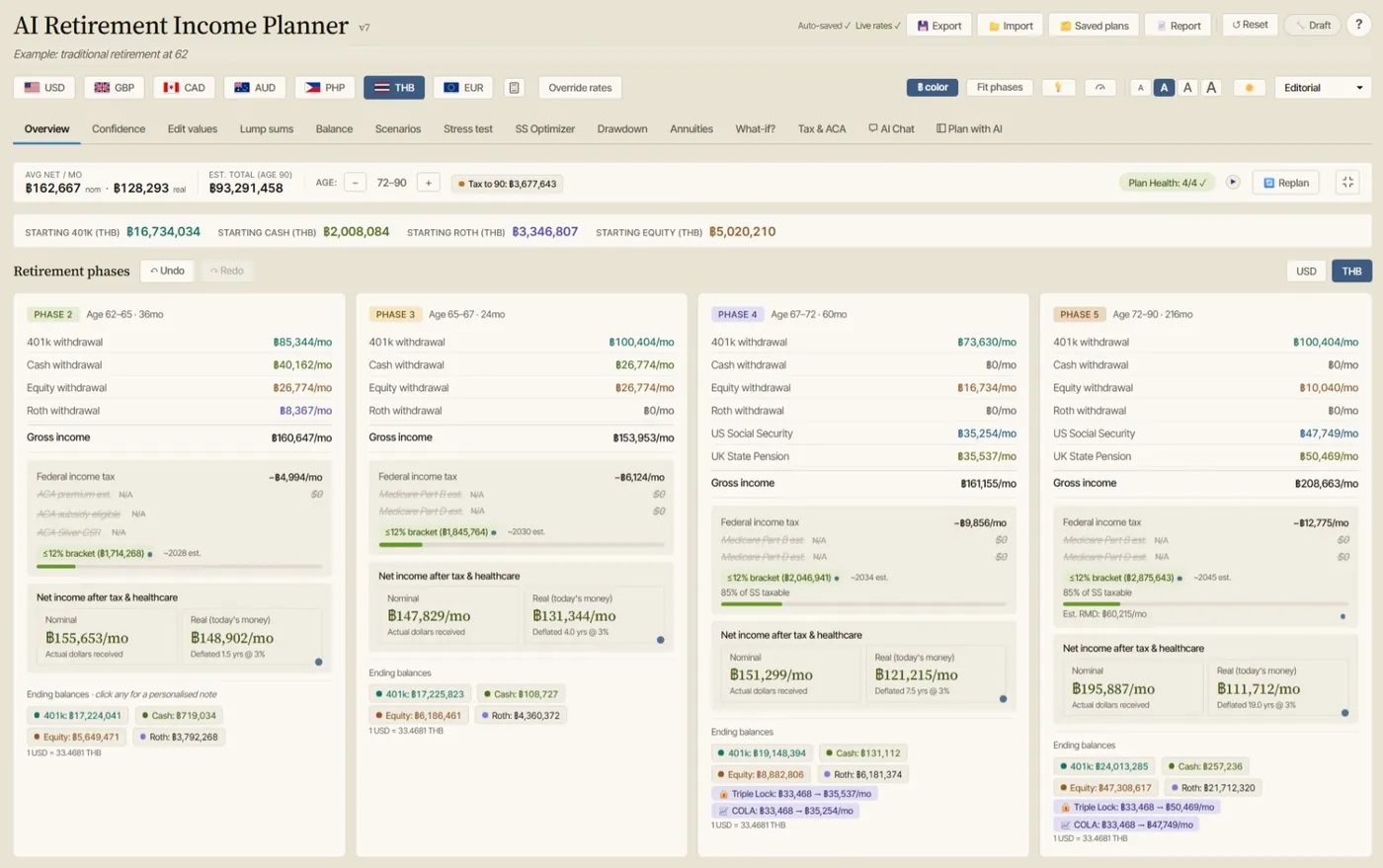

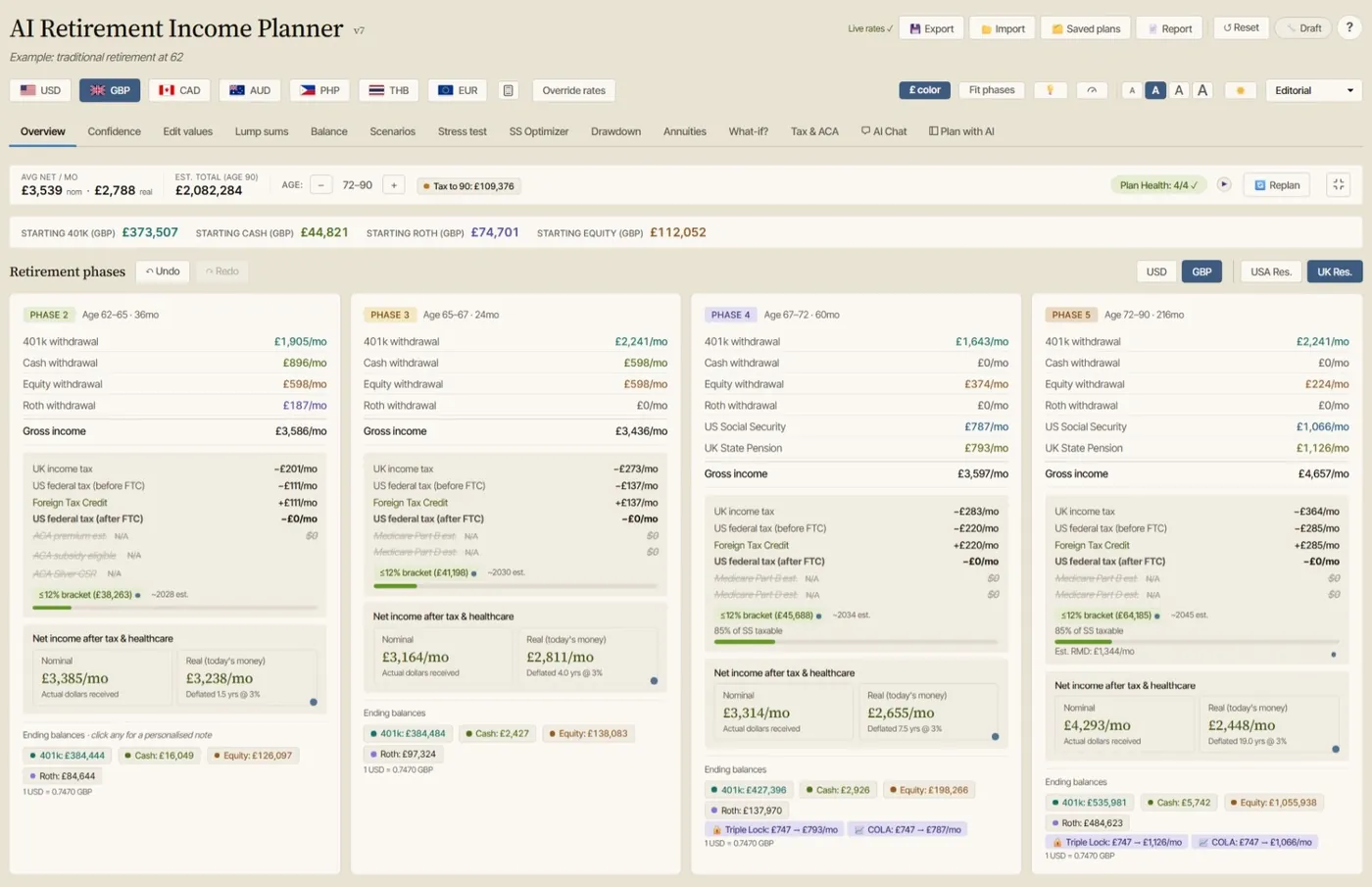

How To Model This In The AI Retirement Income Planner

Use this workflow:

- Build and save the US baseline.

- Duplicate it as the abroad base case.

- Select the planning currency for the abroad scenario.

- Update housing, healthcare, taxes, and travel.

- Add custom exchange-rate assumptions.

- Add foreign-residence healthcare assumptions.

- Add a foreign-account reporting checklist item in notes.

- Save weaker-dollar, higher-healthcare, and return-to-US versions.

- Run Stress Test for each version.

- Compare Plan Health checks.

- Compare Plan Confidence.

- Keep a short list of professional-review questions for tax, visa, healthcare, insurance, and estate planning.

The planner keeps up to three saved plans for side-by-side comparison, so use those slots for the versions you compare most and export any extra variants as JSON backups you can reload later. On the tax side, it models US federal tax and an optional flat state tax, with dedicated resident modes for the United Kingdom, Canada, and Australia (including UK Foreign Tax Credit handling); for other destinations it treats the plan as a US taxpayer or as a foreign resident with US healthcare excluded, so estimate local tax yourself and confirm it with a professional.

The planner is useful because it compares whole retirement plans, not isolated expenses.

Example Comparison

Imagine a couple, ages 64 and 63, deciding between retiring in the United States or abroad at 66.

US baseline:

- Higher housing costs.

- Medicare at 65.

- Familiar healthcare system.

- Federal and state tax.

- Shorter family travel.

- No currency conversion for daily spending.

Abroad base case:

- Lower rent.

- Lower routine care.

- Private healthcare coverage.

- Local spending in another currency.

- More family travel.

- Possible foreign tax.

- Foreign bank account reporting.

Abroad stress case:

- Dollar weakens.

- Healthcare premiums rise.

- One spouse dies.

- Survivor returns to the United States at 79.

The abroad base case may look better. The abroad stress case tells whether that better-looking plan is durable.

FAQ

Is retiring abroad always cheaper than retiring in the US?

No. Some spending categories may be cheaper abroad, but taxes, healthcare, insurance, currency, travel, and return-home costs can change the comparison.

Should I compare after-tax income or gross income?

After-tax income is more useful. Gross income does not show what the household can actually spend after federal tax, state tax, foreign tax, and healthcare costs.

Does Medicare cover retirees abroad?

Medicare usually does not cover healthcare while traveling outside the United States, with limited exceptions. Check Medicare.gov and your specific plan before relying on any coverage assumption.

What is the biggest risk when comparing US retirement and retirement abroad?

The biggest risk is using a single optimistic abroad budget. A better comparison includes taxes, healthcare, currency movement, family travel, survivor planning, and a return-to-US scenario.

Can the planner compare retiring in the US versus abroad?

Yes. The planner can compare saved scenarios across currencies, healthcare assumptions, tax assumptions, exchange-rate assumptions, Stress Test, Plan Health checks, and Plan Confidence.

Source Links

- IRS US citizens and resident aliens abroad: https://www.irs.gov/individuals/international-taxpayers/us-citizens-and-resident-aliens-abroad

- IRS foreign currency and exchange rates: https://www.irs.gov/individuals/international-taxpayers/foreign-currency-and-currency-exchange-rates

- IRS FBAR information: https://www.irs.gov/businesses/small-businesses-self-employed/report-of-foreign-bank-and-financial-accounts-fbar

- SSA payments outside the United States: https://www.ssa.gov/international/payments.html

- Medicare travel outside the United States: https://www.medicare.gov/coverage/travel-outside-the-u.s.

- CDC travel insurance overview: https://wwwnc.cdc.gov/travel/page/insurance

- AI Retirement Income Planner: https://airetirementincomeplanner.com/

Bottom Disclaimer

This article is for general education only. It is not financial, tax, investment, legal, immigration, visa, privacy, cybersecurity, healthcare, insurance, Social Security, Medicare, estate, AI safety, software, or retirement advice. Confirm tax, healthcare, currency, immigration, insurance, account-reporting, Social Security, Medicare, housing, and estate details with official sources and qualified professionals.