Quick Answer

An AI retirement planner should explain verified numbers, organize assumptions, identify missing inputs, compare scenarios, and help users understand tradeoffs. It should not invent benefit amounts, replace tax rules, predict markets, choose investments, pressure users into action, or apply major numeric changes without human review.

The best version of AI retirement planning is calculator-backed. The math engine runs the plan. AI helps the user understand the plan.

Key Takeaways

- AI should explain planner output, not replace the retirement calculator.

- AI should ask for missing assumptions before producing confident explanations.

- AI should keep user approval between any suggestion and any plan change.

- AI should cite official sources for Social Security, tax, healthcare, Medicare, and retirement account rules.

- AI should avoid market predictions, investment promises, privacy overreach, and unsupported certainty.

The Basic Standard

An AI retirement planner should be held to a higher standard than a general chatbot because retirement planning is a high-stakes topic. It can affect spending, taxes, healthcare, Social Security timing, Roth conversions, withdrawals, estate goals, and household confidence.

OpenAI's own ChatGPT FAQ says model outputs can be inaccurate or misleading and that users should check whether responses are accurate. Investor.gov warns that AI can be used in investment fraud and cautions against relying only on AI-generated information for investment decisions.

That does not make AI useless. It means AI should be placed in the right role, which is why a general chatbot is a different tool than a retirement calculator.

Good role:

Explain this retirement scenario and help me find assumptions to verify.

Bad role:

Decide what I should do with my money.

What An AI Retirement Planner Should Do

1. Explain The Plan In Plain English

A retirement planner can produce charts, tables, balances, taxes, and stress-test results. AI can help translate those outputs into a readable explanation.

It should be able to explain:

- Why a balance declines in one phase and stabilizes in another.

- Why Social Security timing changes withdrawals.

- Why Roth conversions can affect taxes, ACA income, IRMAA, and RMDs.

- Why healthcare assumptions matter before and after Medicare.

- Why survivor scenarios can change the plan.

- Why a stress test is weaker than the base case.

The AI should stay tied to the actual planner output. If the chart shows a balance shortfall at age 84, it can explain that pattern. It should not invent a different result.

2. Ask For Missing Inputs

A good AI planner should notice gaps before offering an explanation.

Missing inputs might include:

- Filing status.

- State tax assumption.

- Social Security claiming age.

- Spouse benefit estimate.

- Healthcare cost assumption.

- Retirement start age.

- Cash reserve.

- Roth balance.

- Pension start date.

- Inflation assumption.

- Life expectancy or planning end age.

- Spending changes by phase.

AI should say, "This answer depends on missing assumptions," when those assumptions matter.

3. Compare Scenarios

Retirement planning is usually a comparison problem. The user is not asking for a perfect forecast. The user wants to know how one choice changes the plan.

An AI retirement planner should help compare:

- Claim Social Security at 62, full retirement age, or 70.

- Retire now or work two more years.

- Use a larger Roth conversion or a smaller one.

- Spend more in early retirement or smooth spending.

- Keep more cash or invest more.

- Use a fixed annuity or rely on portfolio withdrawals.

- Move abroad or stay in the United States.

- Plan as a couple or survivor household.

The AI's job is to explain the tradeoff. The planner's job is to calculate the result, which is why a retirement calculator needs to sit underneath any AI explanation.

4. Show The Source Of The Number

Every important number should have an origin.

For example:

- Social Security benefit: official SSA estimate entered by the user.

- RMD estimate: planner calculation based on the selected RMD age and tax-deferred balance.

- ACA-sensitive income: planner tax and healthcare output.

- Medicare IRMAA watch item: planner threshold and lookback logic.

- Retirement balance: month-by-month projection.

- Confidence result: Monte Carlo, historical backtest, checklist, or stress test.

AI should identify whether a number came from the user, the planner, or an outside source. If it cannot tell, it should say so.

5. Flag Official Rules To Verify

AI should point users back to official sources for rules that change or depend on facts.

Useful sources include:

- SSA.gov for Social Security benefits and claiming rules.

- IRS.gov for tax rules, Social Security taxation, retirement accounts, and RMDs.

- HealthCare.gov for Marketplace income rules.

- Medicare.gov and SSA.gov for Medicare enrollment and IRMAA questions.

- Investor.gov for investment risk and fraud education.

AI should not pretend that its answer is the source of law.

6. Support Human Approval

An AI planner may propose changes, but the user should approve them before the plan changes, the same way the planner's own AI proposals are checked against the simulation before you apply them.

Good proposal:

Increase Roth conversion in the pre-RMD phase by $10,000 and dry-run the change so the user can compare taxes, balances, ACA, IRMAA, and Plan Health before applying.

Bad proposal:

Automatically rewrite the plan because the AI thinks the change is better.

Human approval is not friction. It is the control layer.

7. Preserve Privacy

AI should ask for the minimum data needed. It should not request account numbers, passwords, Social Security numbers, full dates of birth, tax return uploads, or bank login details.

A better AI planner lets users calculate locally, then share only sanitized summaries if they choose to use AI.

What An AI Retirement Planner Should Not Do

1. It Should Not Invent Facts

AI should not fill in missing Social Security benefits, tax filing status, healthcare costs, pension start dates, or account balances unless the user gives those assumptions.

If a value is missing, it should ask.

2. It Should Not Predict The Market

An AI retirement planner can explain risk. It should not claim to know next year's return, the next recession date, or which investment will win.

Investor.gov's AI fraud alert warns investors to be careful with AI-related claims and to avoid relying only on AI-generated information for investment decisions.

A better tool uses stress tests, historical backtesting, and Monte Carlo simulation to show ranges and vulnerabilities.

3. It Should Not Replace Official Benefit Estimates

AI should not calculate a user's Social Security benefit from vague work-history details. It should ask the user to get official SSA estimates and enter those into the planner.

It can then explain how Social Security timing affects income, withdrawals, taxes, and survivor planning.

4. It Should Not Turn Tax Planning Into A Guess

AI can explain tax concepts. It should not make tax claims from incomplete facts.

A retirement planner should use structured tax parameters and show the assumptions. The user should verify important tax issues with IRS sources and qualified professionals.

5. It Should Not Hide Uncertainty

Retirement planning has uncertainty:

- Market returns.

- Inflation.

- Healthcare costs.

- Tax law.

- Life expectancy.

- Long-term care needs.

- Family changes.

- Currency changes for international plans.

AI should make uncertainty visible. It should not make uncertain outcomes sound settled.

6. It Should Not Pressure The User

AI should not use urgency, fear, or sales pressure. Investor.gov warns that high-pressure tactics and unrealistic claims are common warning signs in investment scams.

A planning tool should help users compare choices calmly.

7. It Should Not Ignore Data Privacy

AI should not ask for more sensitive data than needed. It should not encourage full document uploads when a summary is enough. It should not treat chat history as a private vault unless the provider's settings and policies support that claim.

Buyer Checklist For AI Retirement Planners

Use this checklist when evaluating an AI retirement planning tool.

Calculation

- Does it have a real planning engine?

- Does it model taxes, healthcare, Social Security, pensions, withdrawals, and balances?

- Does it run scenarios rather than giving one answer?

- Does it include stress tests or confidence measures?

- Does it show assumptions clearly?

AI Behavior

- Does AI explain output from the calculator?

- Does AI ask for missing assumptions?

- Does AI identify uncertainty?

- Does AI avoid market predictions?

- Does AI keep major changes under user approval?

- Does AI separate explanation from action?

Privacy

- Does the tool require an account?

- Does it connect to banks or brokerages?

- Where is plan data stored?

- Are exports controlled by the user?

- Are AI features optional?

- Can local AI be used?

- Are network calls explained?

Verification

- Does the tool point users to SSA, IRS, HealthCare.gov, Medicare, or Investor.gov when rules matter?

- Does it identify when a professional review may be needed?

- Does it avoid certainty when laws or assumptions may change?

How The AI Retirement Income Planner Fits

The AI Retirement Income Planner follows a calculator-first model.

Confirmed planner capabilities include:

- Month-by-month retirement income projection.

- Social Security and spouse Social Security inputs.

- Social Security claiming comparison from 62 to 70.

- Couple claiming strategy search.

- Pensions, rental/passive income, part-time income, lump sums, and fixed annuity income.

- US federal tax parameters, taxable Social Security calculation, optional flat state tax, ACA, Medicare, and IRMAA, RMD estimates, and Roth conversions by phase.

- Balance and income charts.

- Scenario comparison.

- Stress Test.

- Drawdown strategy comparison.

- Monte Carlo simulation.

- Historical backtesting.

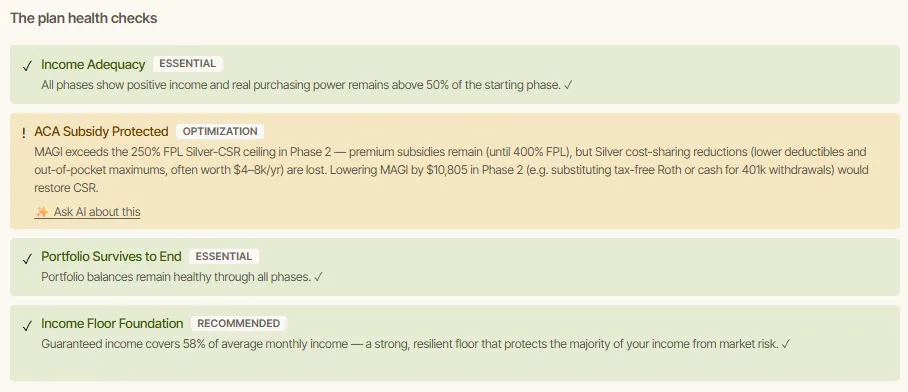

- Plan Health checks.

- Plan Confidence dashboard.

- Report preview.

- Optional AI Chat and Plan with AI sidebar.

- User-reviewed AI proposal workflows.

- Manual JSON export/import and up to three saved plan slots.

Important privacy and network wording:

- It is a single self-contained HTML file.

- It runs locally in a modern browser once opened.

- It does not require a planner account.

- It does not aggregate bank, brokerage, payroll, or account data.

- Plan data is stored in browser localStorage.

- Optional AI/API features and exchange-rate fetching can make network calls when the user chooses.

- Ollama can be used as a local AI option.

That structure supports the safer pattern: calculate first, explain second, approve changes yourself.

A Practical Prompt

Use this prompt when testing an AI retirement planner:

Using only my planner output, explain this scenario in plain English. Do not make investment, tax, legal, Social Security, Medicare, insurance, or healthcare decisions for me — just explain.

For each important number, say where it came from. Flag the biggest tradeoffs and any missing assumptions, and note what I should verify with an official source. Suggest what to test next, but do not apply any changes unless I approve them first.

This prompt puts AI in the right chair.

FAQ

Should an AI retirement planner calculate the whole plan by itself?

No. The better structure is a calculator-backed planner with AI explanation layered on top. The retirement engine should handle the math, assumptions, and scenarios.

What should AI be best at in retirement planning?

AI is most useful for explanation, assumption review, scenario summaries, plain-English reports, missing-input checks, and question preparation.

What should AI avoid?

AI should avoid inventing facts, predicting markets, replacing official sources, making tax conclusions from incomplete data, pressuring the user, or applying major changes without approval.

Why does human approval matter?

Human approval keeps the user in control. It lets AI suggest or explain, while the user reviews the numbers before any change affects the plan.

Can AI help with Social Security, Roth conversions, and withdrawals?

Yes, if it works from verified planner outputs. It can explain timing and tradeoffs, but official rules and personal decisions still need verification.

How can I tell if an AI retirement planner is overpromising?

Be cautious if it claims certainty, predicts markets, ignores assumptions, asks for excessive private data, or promises unusually strong investment outcomes.

Source Links

- OpenAI Help Center, What is ChatGPT?: https://help.openai.com/en/articles/6783457-chatgpt-general-faq

- OpenAI Help Center, Data Controls FAQ: https://help.openai.com/en/articles/7730893-data-controls-faq

- Investor.gov, Artificial Intelligence and Investment Fraud: Investor Alert: https://www.investor.gov/introduction-investing/general-resources/news-alerts/alerts-bulletins/investor-alerts/artificial-intelligence-fraud

- Investor.gov, What is Risk?: https://www.investor.gov/introduction-investing/investing-basics/what-risk

- FTC Consumer Advice, Protect Your Personal Information From Hackers and Scammers: https://consumer.ftc.gov/articles/protect-your-personal-information-hackers-and-scammers

- AI Retirement Income Planner: https://airetirementincomeplanner.com/

Bottom Disclaimer

This article is for general education only. It is not financial, tax, investment, legal, privacy, cybersecurity, healthcare, insurance, Social Security, Medicare, estate, AI safety, software, or retirement advice. AI output can be inaccurate or misleading, and retirement planning decisions should be verified with reliable sources and qualified professionals.